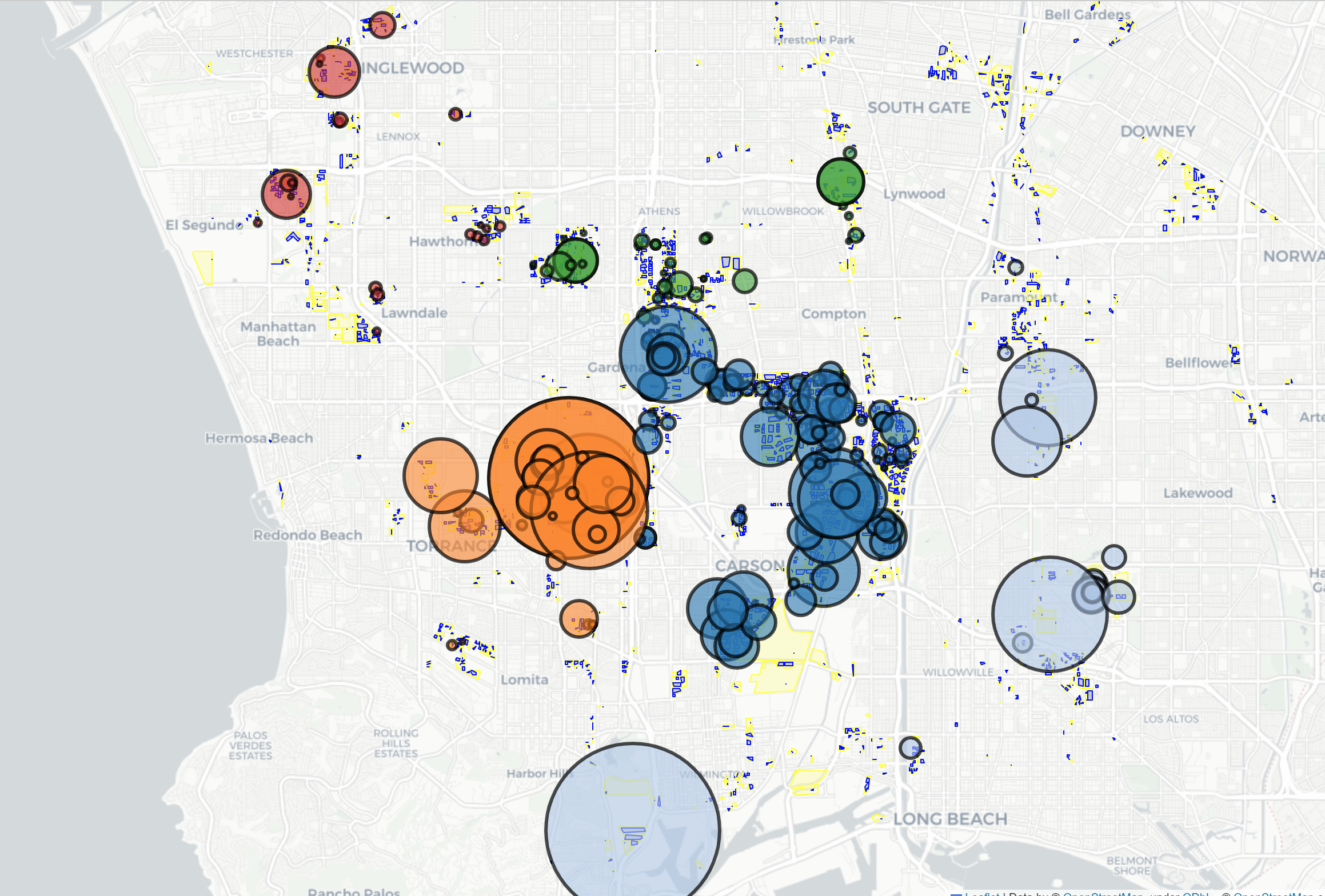

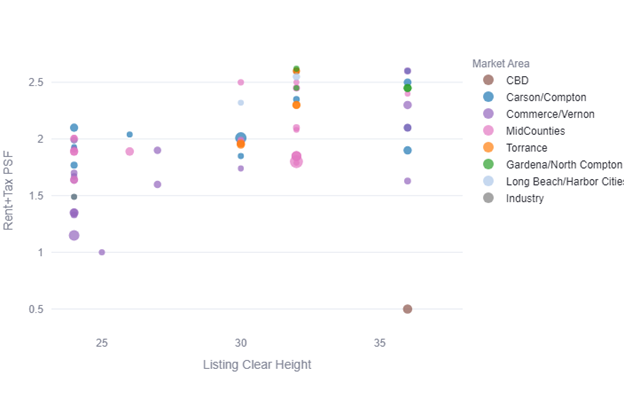

Despite higher than normal industrial vacancies, Hard Tech companies are finding it difficult to locate adequate industrial space. Many Hard Tech companies require substantial electical power. They want a free-standing building for U.S. Government clearance, more office space than is typical, a large parking area, and a location to attract engineers. Many Hard Tech companies prefer El Segundo and neighboring beach communities because of its history of aerospace and defense manufacturing. But they will consider other locatons along the 405 corridor from LAX to Irvine, including Torrance, Long Beach and other locations in Orange County. Some Hard Tech Companies will make the difficult decision to split their manufacturing from engineering to find the right facility in the location they want. Other parts of Los Angeles that served as machining centers in the past are located in Gardena/Carson, Commerce/Vernon and parts of the San Fernando Valley. Following are a couple of graphs describing market conditions:

Offerings are scarce in the El Segundo/Beach Cities area. When Hard Tech companies grow, they often look to Torrance, Hawthorne, Gardena, Carson or Long Beach. These cities are close to experienced engineers and they house good production facilities.

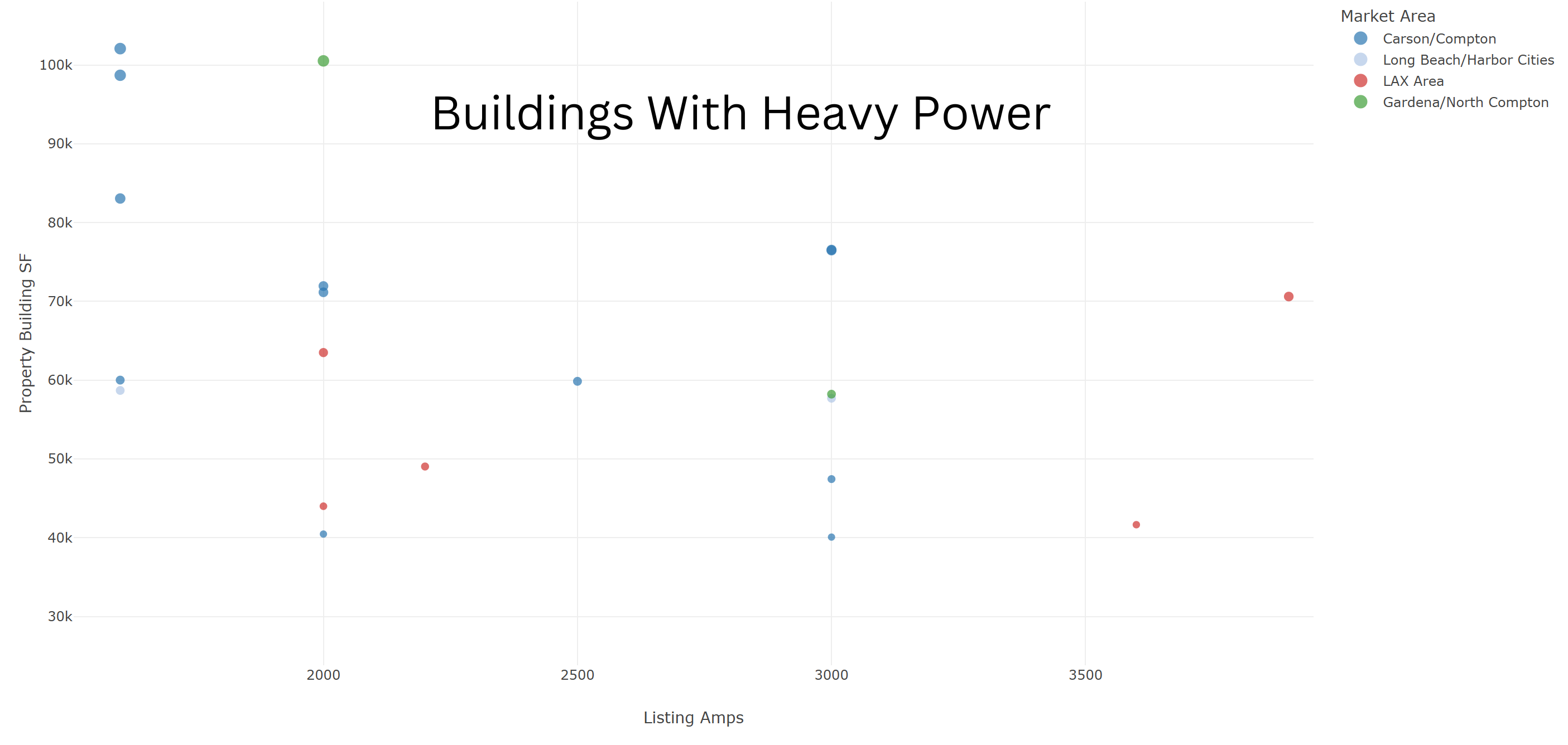

Power is a main criteria for many Hard Tech Companies. If you need heavy power, 2000 AMPs or greater, there are only a few buildings with the necessary capacity in each square foot range.

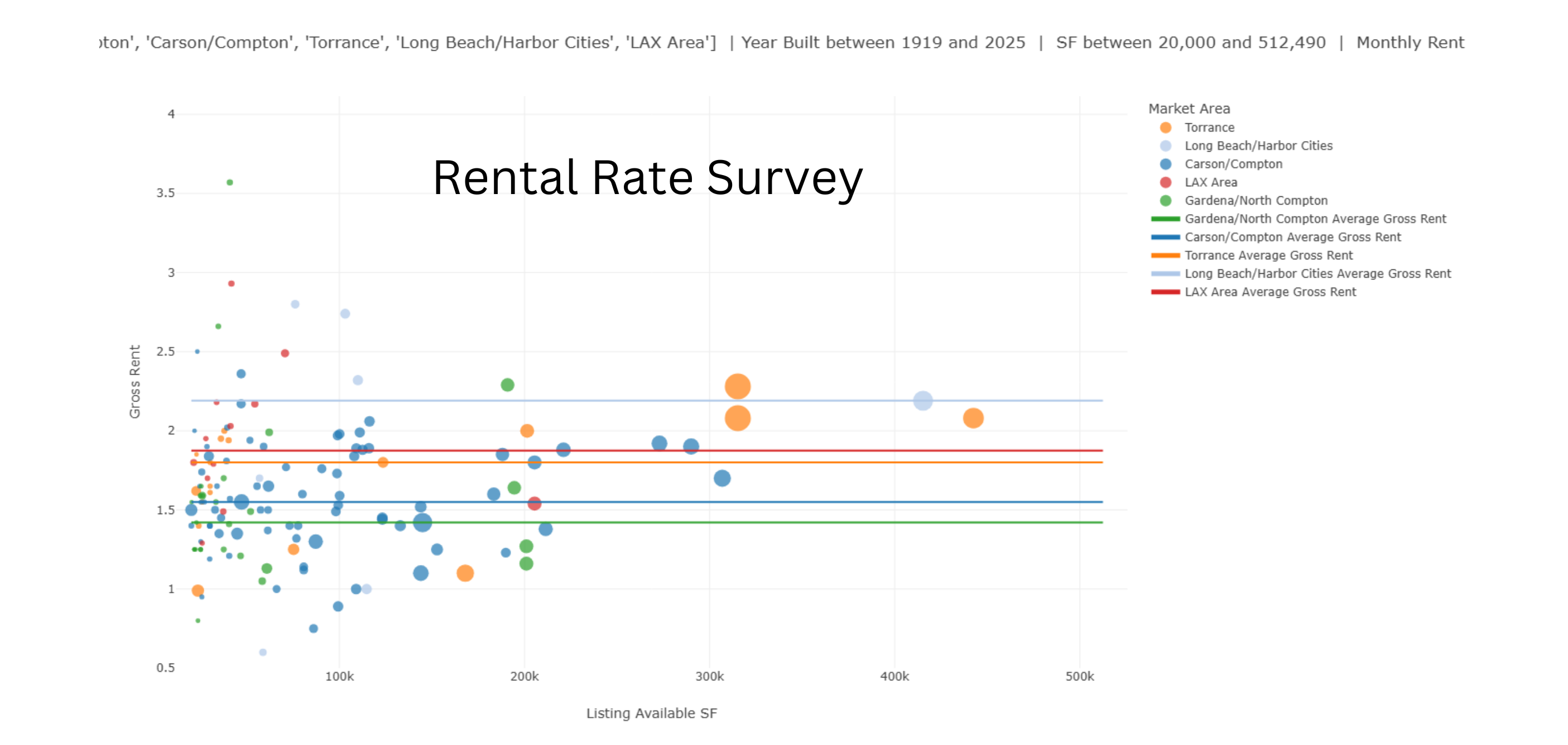

Rents hover between $1.50 to $2.25 Gross per square foot per month depending on location and amenities.

If you are seeking a new building or have questions about Los Angeles industrial real estate, please contact us today.

The Los Angeles industrial real estate market is financialized. That means pricing reflects accepted investment principles. Investment buyers, flush with private capital, are searching for smaller and older buildings than what you would normally expect from fund level buyers. Assets owned by individuals, corporations, families, and partnerships are being sold to large investment groups, funds, and REITS. It started with “Class A” buildings but escalated for almost all industrial buildings with low interest rates after the Great Financial Crisis. Activity surged during Covid, levelled off during the recent period of higher interest rates, and is regaining strength with more capital allocations hitting almost all industrial properties that generate long-lasting income.

In our experience, some building owners prefer comprehensive marketing and others want discretion. We developed our resources to do both:

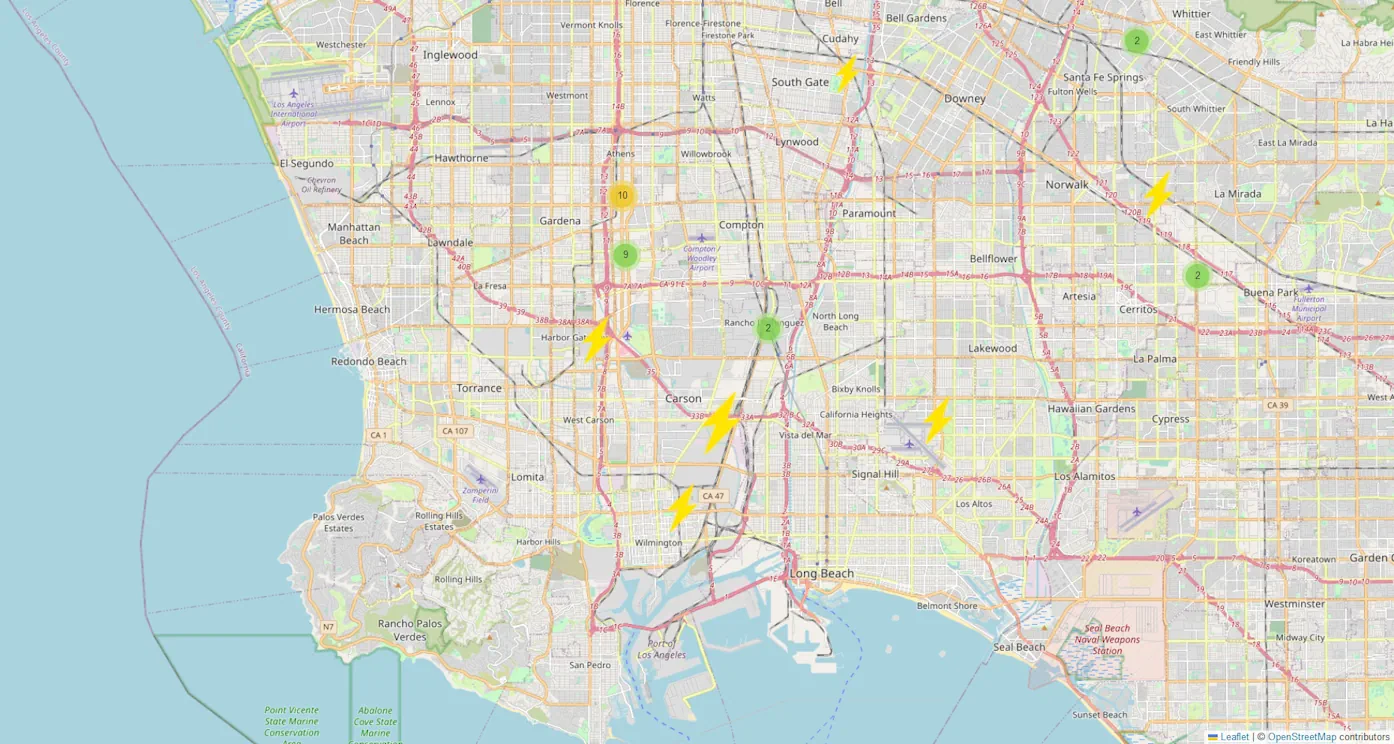

In less than 18 months, the industrial building market has shifted from low vacancy to abundancy. There are now 215 industrial spaces, greater than 50,000 square feet, available in the Greater Los Angeles Basin. This does not include Orange County, Inland Empire, or San Fernando Valley. Only the areas you see on the map (below). About 20% is sublease space.

The best value for most tenants is second and third generation spaces. Many of these buildings built since the year 2000 have the same characteristics as brand-new buildings except for ceiling heights, although many of these 2nd Gen buildings still go to 30’.

36’ high buildings came in around 2023

30’ – 32’ Clear was the norm starting in 2000

24’ Clear started as far back as 1975

Older buildings are equally functional as new buildings for less rent, especially if they have a low tax basis. One exception is if the tenant plans to install interior warehouse installations like mezzanines or specialty racking and automation. In these cases, latest generation buildings have an economic advantage because of height.

Some of the calculations we perform to determine functionality include:

Location and Distance

Docks per 10,000 SF

Building to land ratio

Cubic Capacity and Cost per Cube

Property Taxes/Expenses

Ceiling height

Sublease

To identify the better buildings, we subject all available properties through a macro analysis. This is the best way to identify differences in functionality and cost when there are a lot of choices.

Here is an example:

Let’s say you are in 100,000 square feet in the South Bay and you want to double in size. Some tenants will move completely to put everything under one roof. Other tenants will look for a satellite building as an interim step. Most South Bay companies will look locally and as far as Santa Fe Springs and Mid Counties. Some will want to go as far as IE West. What will you find?

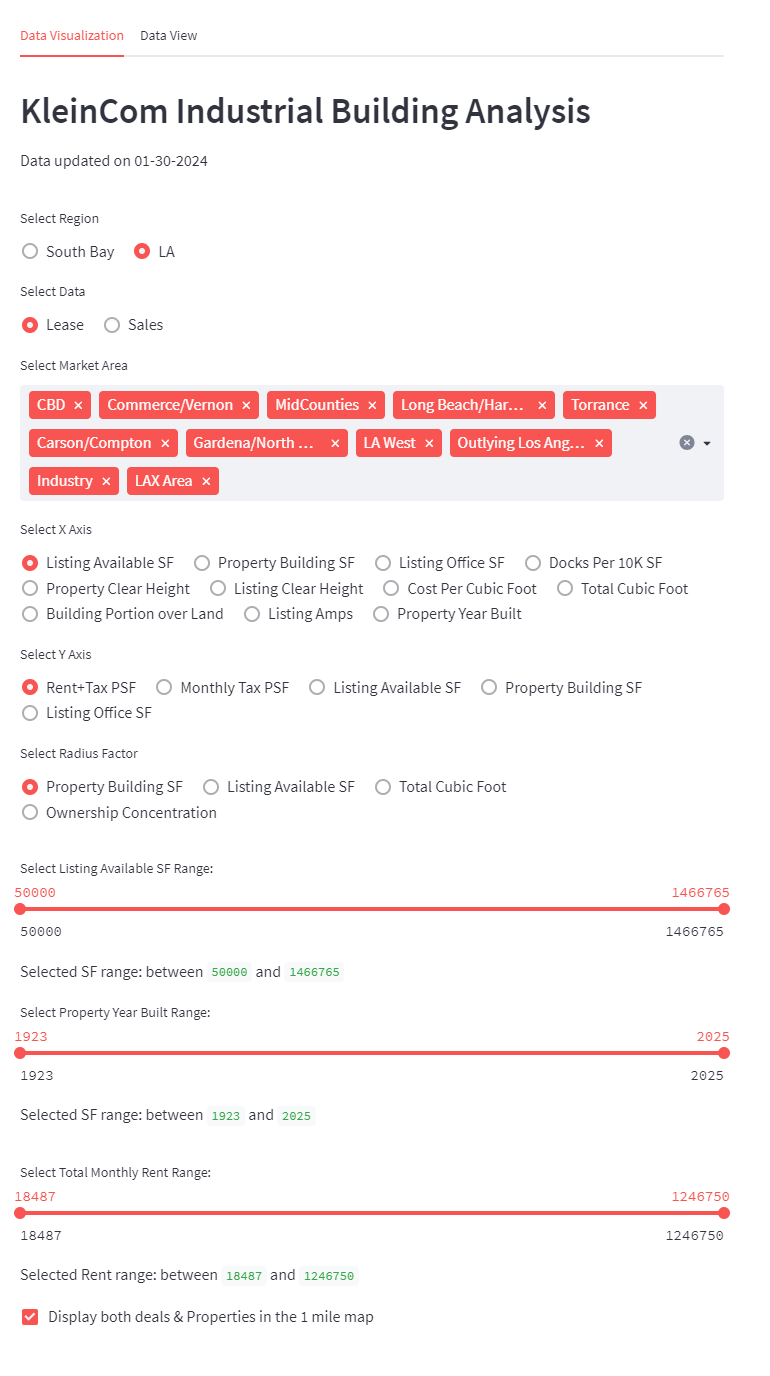

Streamlit Demo View

We model the entire market on the Kleincom Industrial Building Analysis we developed on Streamlit. For this report (100,000 SF to 250,000 SF), we identify 55 choices of which 14 are subleases with terms of at least 3 years (some up to 5). For demonstration purposes, we will leave aside, the additional 80 or so buildings in Inland Empire West (Rancho Cucomonga, Ontario, Chino, and Fontana) that meet the size requirement.

Using Ceiling Height with 24’ as the minimum, we establish the following distribution. For most tenants, 30’ to 32’ is the sweet spot.

All Buildings 100K to 250K

Buildings are dispersed over the entire Los Angeles Region.

Buildings 100k to 250K L.A. Basin

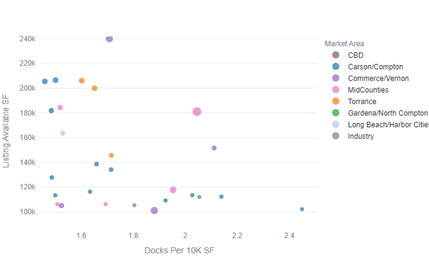

The second factor to sort the choices is the Loading Dock Ratio measuring docks per 10,000 square feet to determine loading efficiency. Any dock ratio greater than 1.5 doors/10,000 square feet is considered highly efficient and closer to 2 docks/10,000 SF is superior.

Docks Per 10k SF

Looking at the top results, it’s not always the newest buildings that are the best choices. You can lease 2nd or 3rd generation buildings for $1.75 to $1.95 per foot (all-in). About half of the buildings are 30’ or greater.

Results Table

Market Area

Size

Rate

Month

Clr

Year

Cubic Ft

Dock Ratio

B:L

Gardena/ Compton

300000

1.6

$480,000

26

1987

7800000

3.33

40%

Carson/Compton

300000

1.53

$459,000

25

1970

7500000

1.84

52%

Carson/Compton

285000

2.2

$627,000

32

2006

9120000

2.24

41%

Carson/Compton

250000

1.51

$377,500

25

1972

6250000

2.17

60%

MidCounties

250000

1.8

$450,000

32

2002

8000000

2.05

59%

Carson/Compton

150000

2.1

$315,000

36

2024

5400000

2.84

60%

Commerce/Vernon

150000

2.6

$390,000

36

2024

5400000

2.11

55%

For some tenant’s subleases may be the right answer because the terms are relatively short, and the financial commitment will be less. Ecommerce tenants and larger Amazon/Temu Sellers are drawn to subleases. The top subleases have exceptional loading and low property taxes. In most cases, landlords will renew when the lease expires.

Best Subleases

City

SF

Yr Blt

HGT

DH

Dock Ratio

Years Remaining

Carson

300000

1973

22

40

1.33

3.69

Industry

225000

1996

30

25

1.11

5.58

Torrance

200000

2000

30

30

1.50

2.69

Torrance

135000

2001

30

25

1.85

3.44

Commerce

125000

1957

22

55

4.40

5.28

Santa Fe Springs

120000

2003

30

30

2.50

3.78

La Mirada

100000

1997

30

20

2.00

2.44

Compton

100000

1981

24

15

1.50

3.02

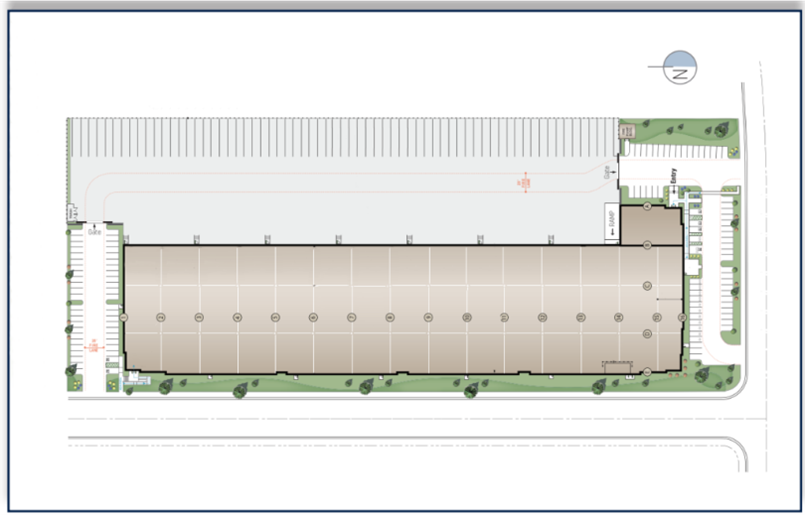

Experienced tenants will use site plans to decide. There is a preference for a more rectangular building than a square so you can load more trucks simultaneously and divided to sub-customers if necessary. Here’s an example of two buildings of approximately the same size and asking rent. Most tenants would prefer the first building because loading exceeds 2 docks per 10,000 square feet, it has additional trailer parking, and the warehouse can be easily divided into sections while maintaining optimum functionality.

The second site plan is reasonably functional but only has 1 dock per 10,000 square feet, can only be divided in half and is less functional than the first example. For the same cost, most tenants will choose the first building.

With the high cost of land and construction costs, developers need to maximize building coverage to compete and make a profit. In other words, developers are often forced to build the largest possible building on the site while doing their best to keep the building functional. As you can see, some buildings are more functional than others.

Every tenant has different priorities, but most revolve around the same criteria of location and function. At Klein Commercial, we have 40 years of corporate real estate experience locating the best buildings for our clients. Our latest tool, the Kleincom Industrial Building Analysis, will help you make the best choice amongst all the available space on the market today.

Industrial real estate is a diverse business that includes Investment funds, developers, private/family owners, corporations, occupiers, and a mix of product types and industries. Industrial buildings are in every community and are the source of employment, production, distribution, and wealth for many. The nation’s economic health rides on the success of industrial real estate.

There are several factors that are driving deals today. Broadly, these include Interest Rate Policy, US Industrial Strategy, and Local Municipal Governance. Everyone is affected differently. For example, higher interest rates are never good for real estate, though they affect sales more than leases; sale transactions are interest rate sensitive while leasing is supply and demand based. As an experienced broker, we use detailed knowledge, market analytics, and long-standing relationships to help you in making the best decision. Continue reading “How Is Industrial Real Estate Today?”

I could not start the year without acknowledging the tools that are currently available at Open AI. I’ve recently created a new FAQ page with the use of ChatGPT and Dall-E 2. It must have been under the wire before Google Search created new defenses against text bots. I received one solid lead from a company looking for 30,000 square feet because of the AI-generated explanation of my services. Continue reading “Three Innovations for 2023”

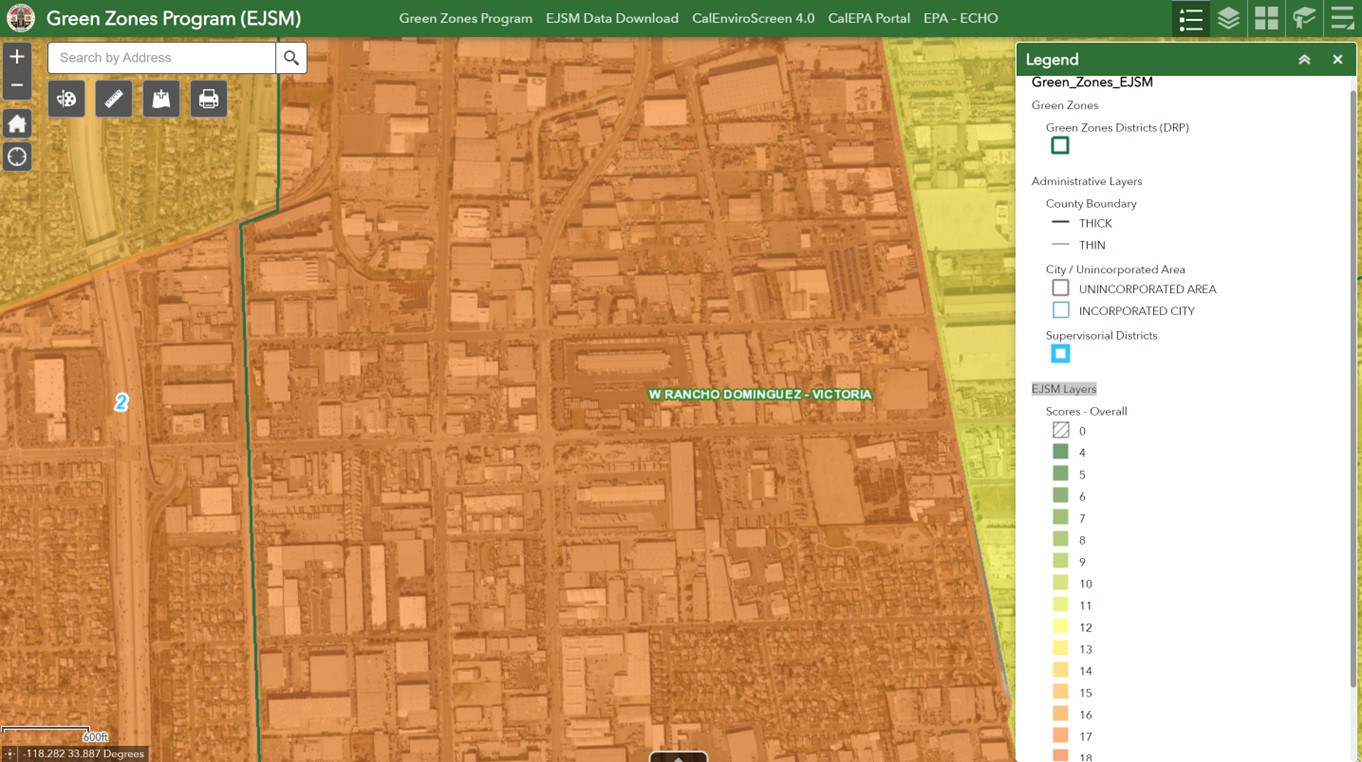

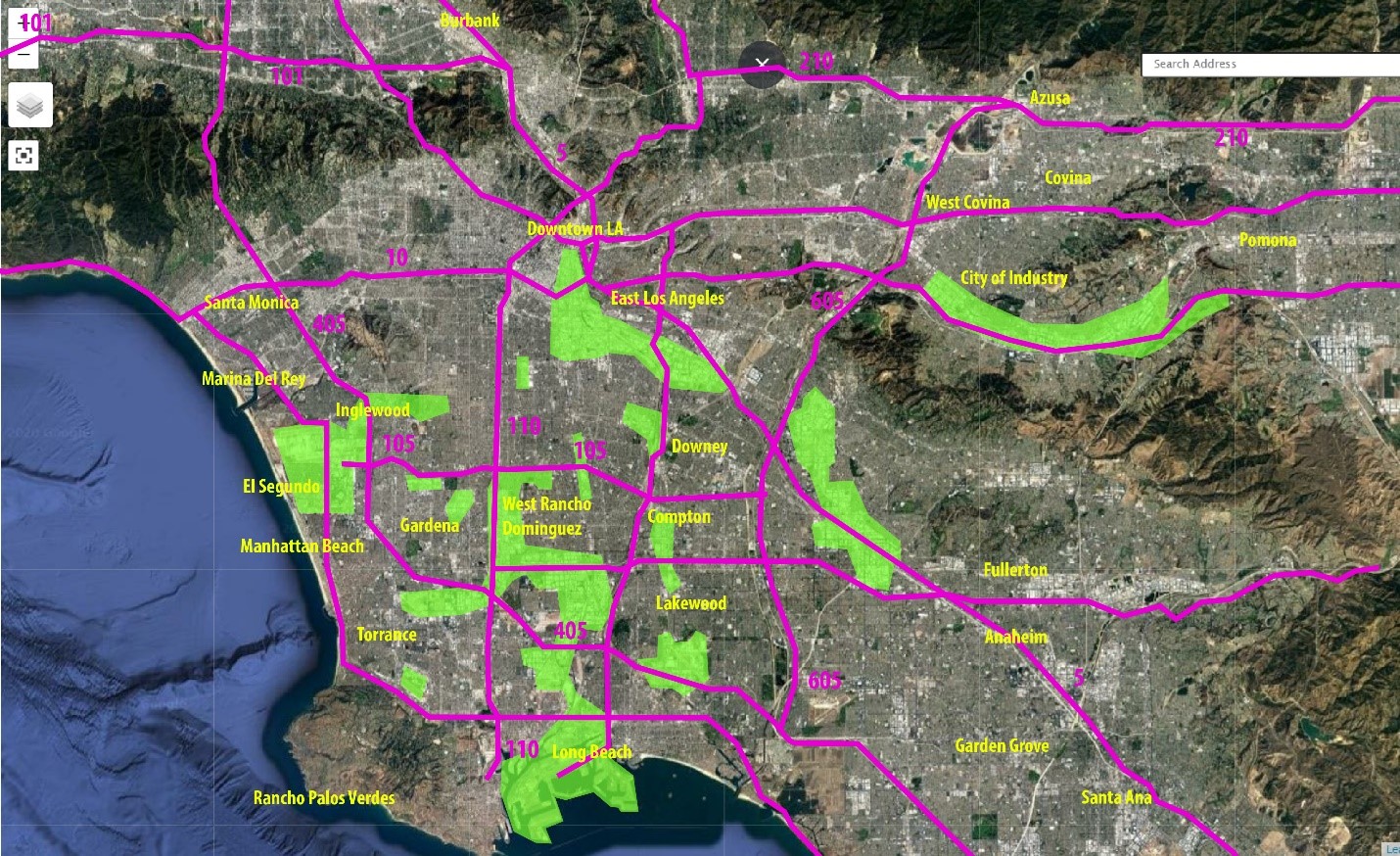

Leasing Industrial Property in Los Angeles County Under the New Green Zone Ordinance

Green Zones

Green Zones are an entirely different way to look at zoning. It is an outgrowth of the Environmental Justice Movement that had its local origins addressing diesel exhaust at the Port Complex in San Pedro Bay. Properties are analyzed and graded based on their contribution to health disparities using the Environmental Justice Screening Method (EJSM). The EJSM is a new tool and strategy that is designed to correct unhealthy conditions by establishing new mitigation mechanisms. The County will use the EJSM for ongoing monitoring and annual reporting to the parcel level.

Depending on the EJSM score, Regional Planning offers four (4) different routes to approval. The simplest is Site Plan Review (SPR) and it is approved administratively in what we use to call, “over the counter”. The other three routes are discretionary and require formal application and Public Hearing at different levels of planning authority. Generally, the greater the health impact, the longer the approvals. Continue reading “Leasing Industrial Property in Los Angeles County Under the New Green Zone Ordinance”

For the past several years, and particularly during the COVID-19 Period, conventional underwriting took a back seat to momentum. No one’s pro-forma predicted the incredible rent growth over this period. Low interest rates and shortage of product drove prices higher. Industrial rents doubled in two years. Underwriting was limited to the simple and liberal measurement of Net Rent/Purchase Price = Rate of Return. Any return higher than treasury rates signaled a buy. It was the period of “Search for Yield”. Continue reading “Stricter Underwriting is Here – Industrial Policy is a New Catalyst”

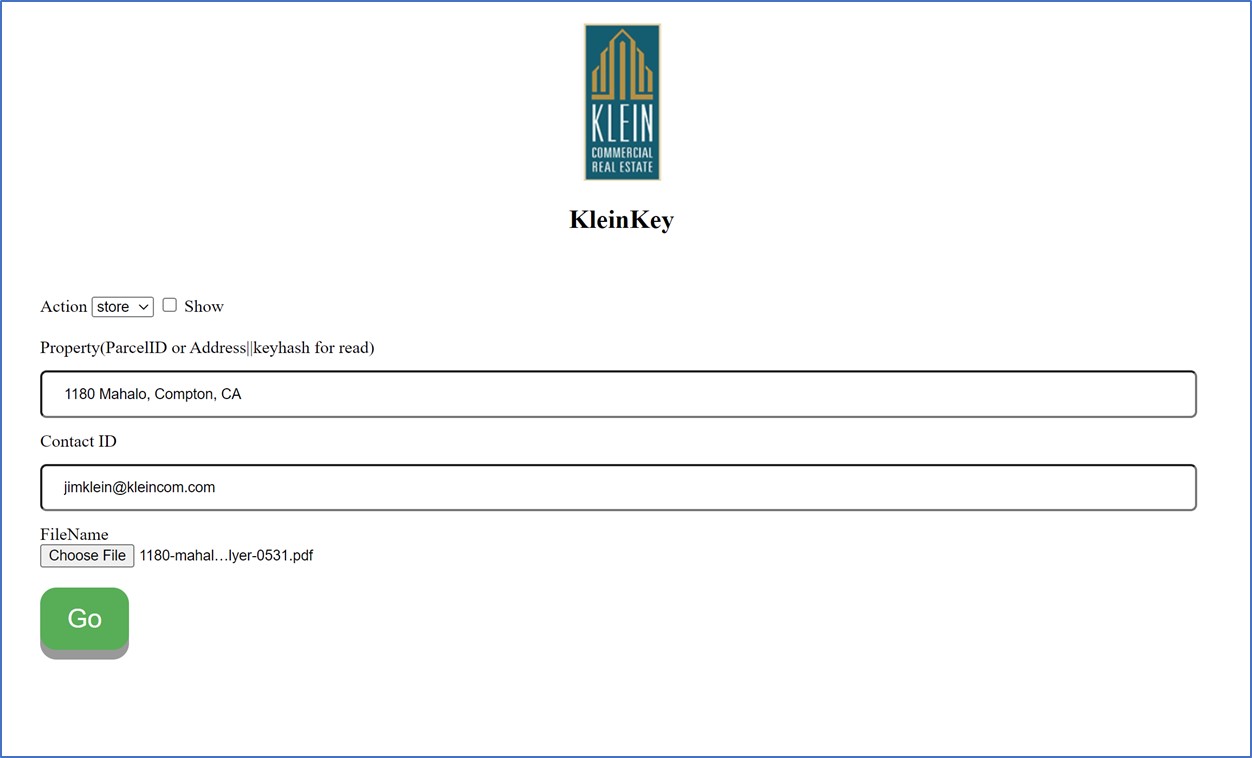

Putting a property on the blockchain allows people to transact if they have the link. When we post a property, the blockchain generates a cryptographic key which allows the possessor access to the property. We give that key, in the form of a link or a QR code. There are associated rights with the key that are compared to an NFT or a token, but our purpose for using the blockchain is its ordering system. The key is only sent to Selected Trusted Parties that are registered or known. Nothing is posted online or in the Multiple Listing Services because blockchain is used for privacy. Continue reading “Blockchain: Should You Post Your Industrial Property?”