It’s 2025 and It Will Never Be The Same

In North Santa Monica, where I reside, we are the lucky ones. Destruction from the fires is just over the ridge. We can walk down the staircase on Adelaide, pass Canyon Elementary, climb back up Rustic Canyon, and be in the center of the burn area in a 15-minute hike. It’s smoky, many residents have left the streets to quiet. Face masks are common and the color of the sky is a tinge of orange. Threats of more wind are in the offing. Today, large convoys of police cars and fire trucks, 15 or 20 in a group, are traveling up the 405 with flashing lights to pre-position.

When we evacuated on the first night, we came to the New Gardena Hotel. It’s Japanese-owned and managed with high standards and a good breakfast. It’s in the center of the Gardena restaurant row with noodles, seafood, Japanese, Korean, and Vietnamese delicacies across the street at Pacific Square and Tozai Plaza. I saw a customer at the hotel who did the same as us, to be near his business. His house was destroyed.

Today is President’s Trump inauguration day in Washington D.C. It will bring a new era of governing. The administrative state will be top of the agenda. If you’ve dealt with local planning agencies and the mounds of restrictions from Green Zone Ordinances, buffer zones, AB 98, Environmental Justice, and other anti-industrial building measures, you can see how far astray local leaders have gone by neglecting basic municipal services. The other initiatives I’ll be watching will be AI, Crypto, and Super Intelligence. These are new agencies headed by talented and experienced executives with histories of founding tech companies. And limited Regulation!

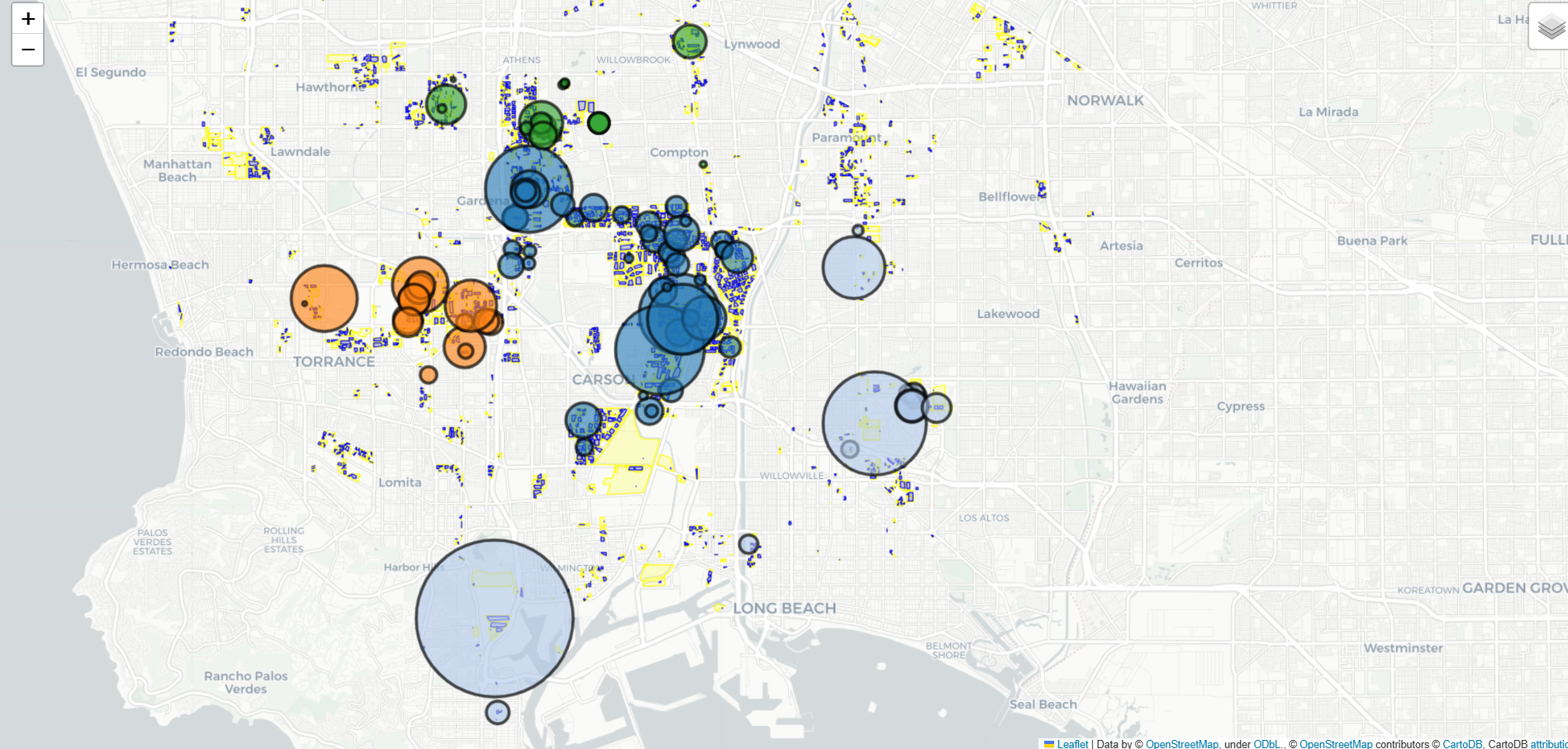

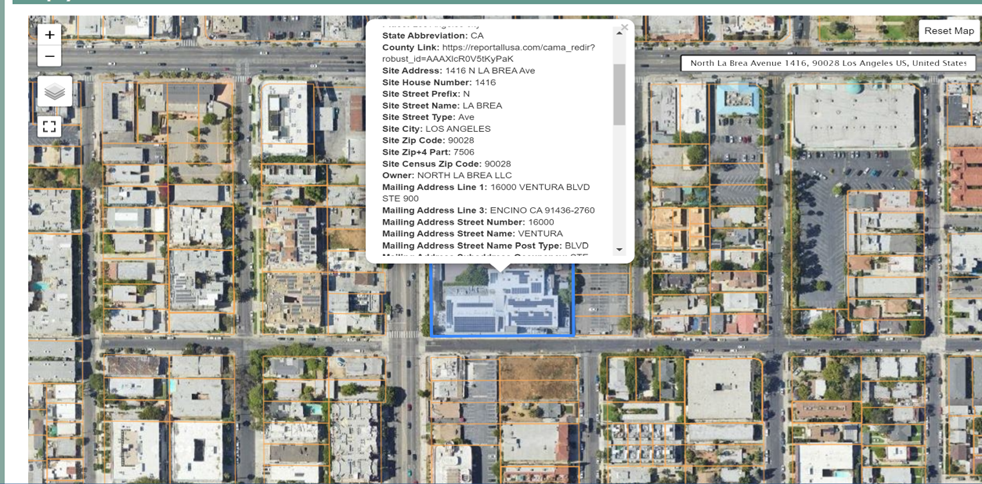

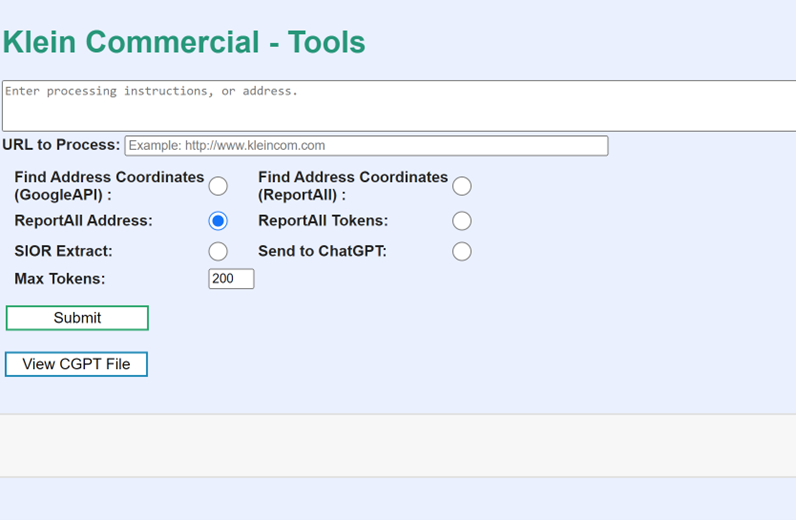

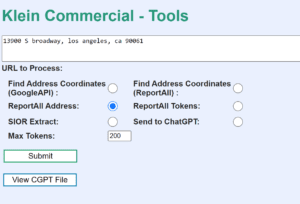

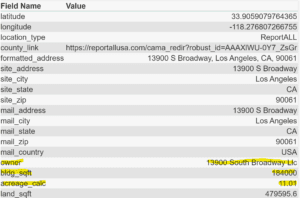

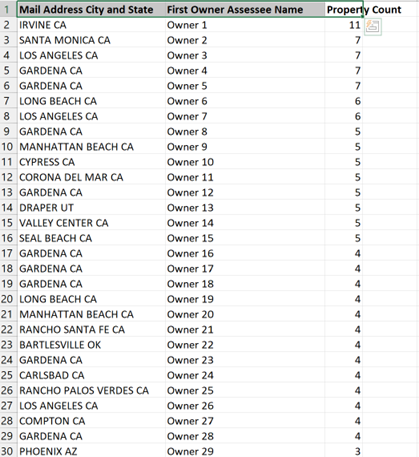

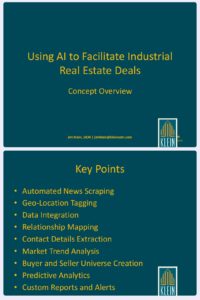

AI is the transforming technology of a generation. Already, AI chat applications provide learning, automation, and useful outputs that merit continual dialog with your AI pal. At our office, we are preparing for the AI future by cleaning our data (parcel records, salesforce, available, and specialty niches) so it can be read by machines. We geolocate each property and create a unique link to build and show relationships. We focus on local properties, especially those that are potential transactions. We follow certain industries and share techniques with colleagues in different markets.

Crypto is a step to the future. An increase in the value of coins and an embrace of crypto by key finance legislators will bring wider acceptance and knowledge. We experimented by building a blockchain on Hyperledger, but we didn’t have enough transactions to justify the instance cost. Now, we are using IPFS, a public decentralized blockchain where cost is low. In Los Angeles, because many properties trade off-market, in quiet transactions, or under new Buyer regulations, there is a blockchain use case to order and provide certainty. Blockchain is helpful when Sellers want to be discrete. You need not trade crypto coins or speculate to use blockchains. Please look for further explanation of how we use IPFS with customary brokerage procedures

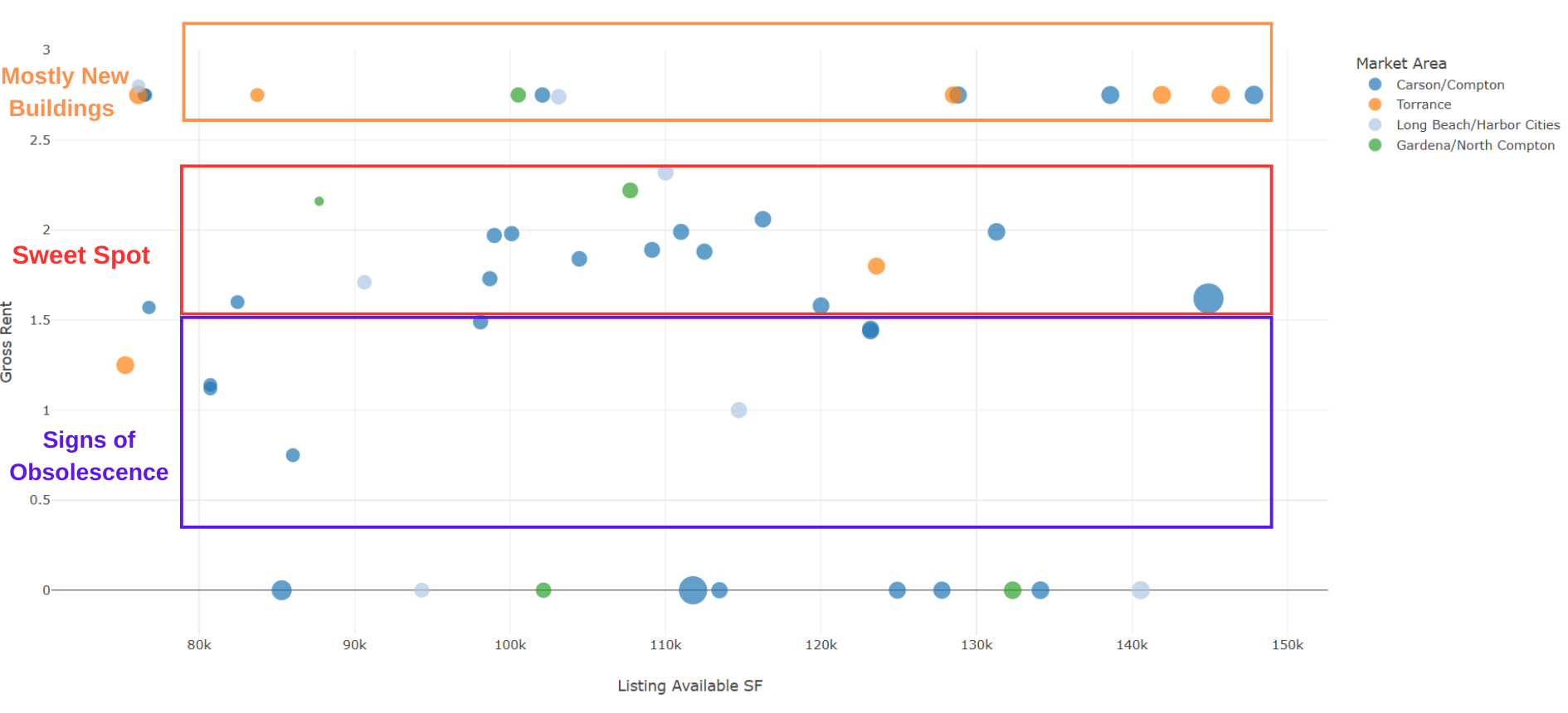

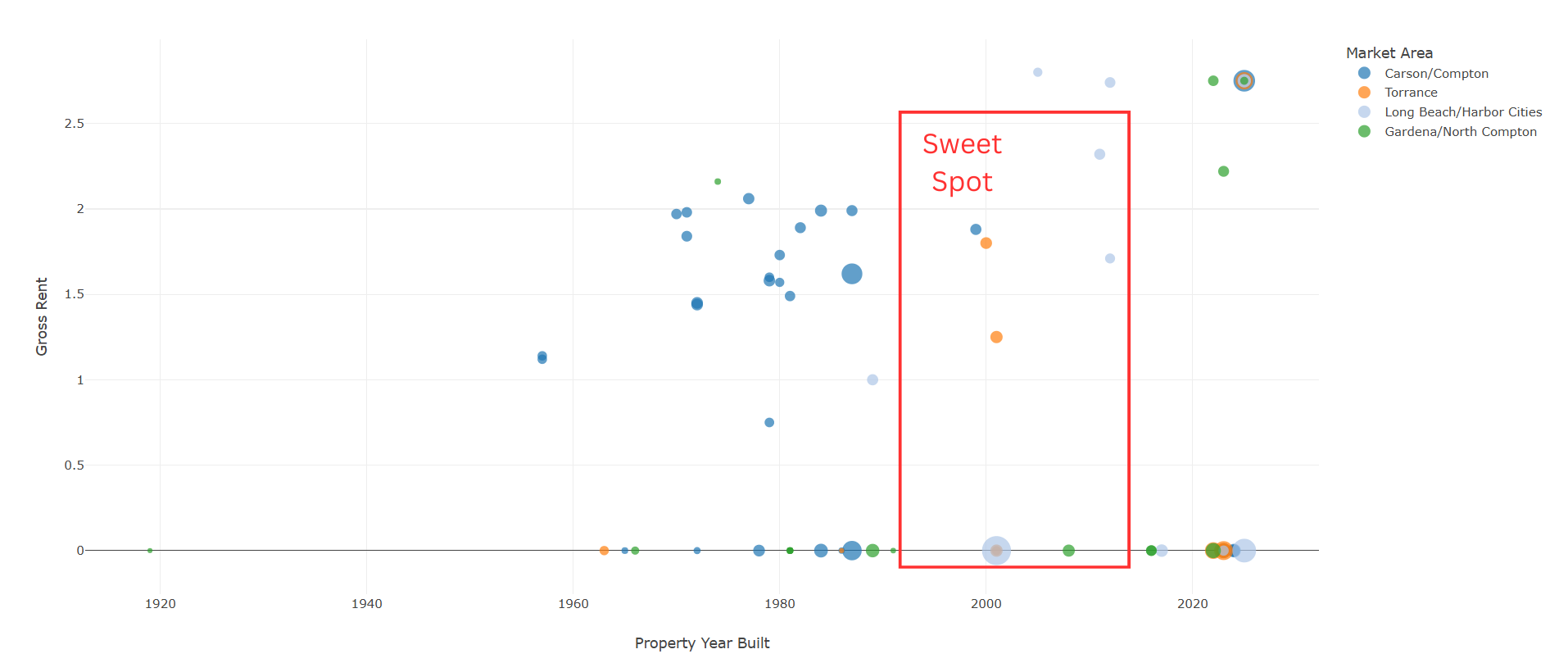

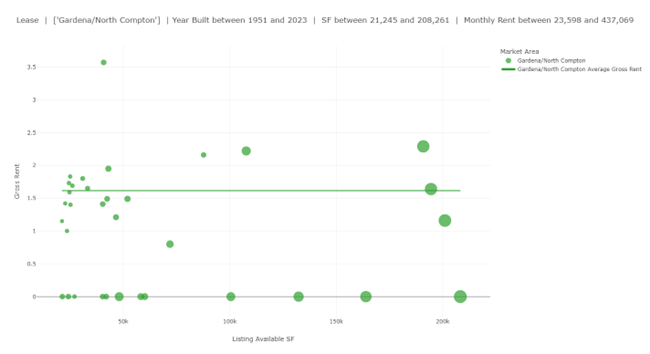

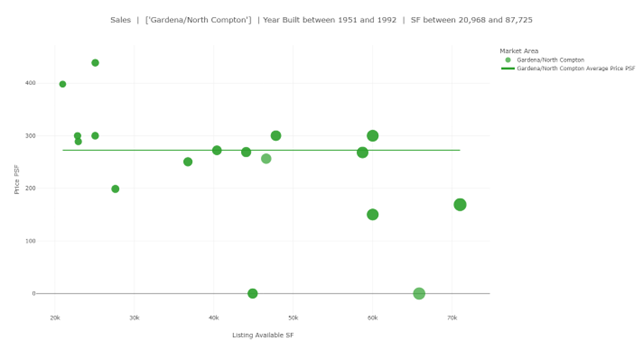

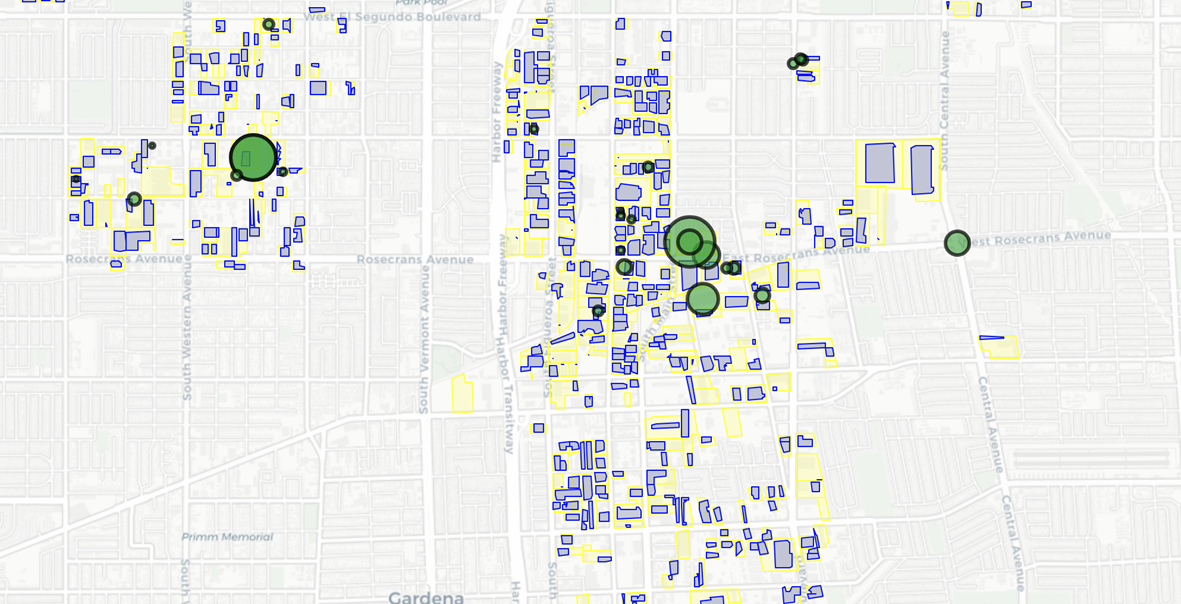

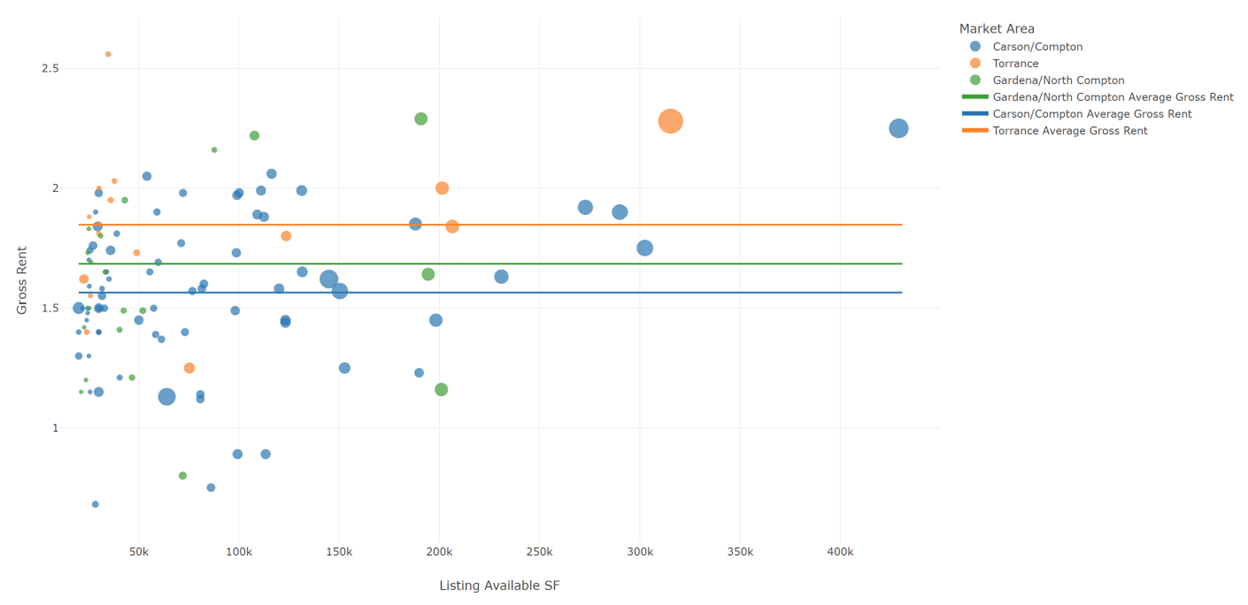

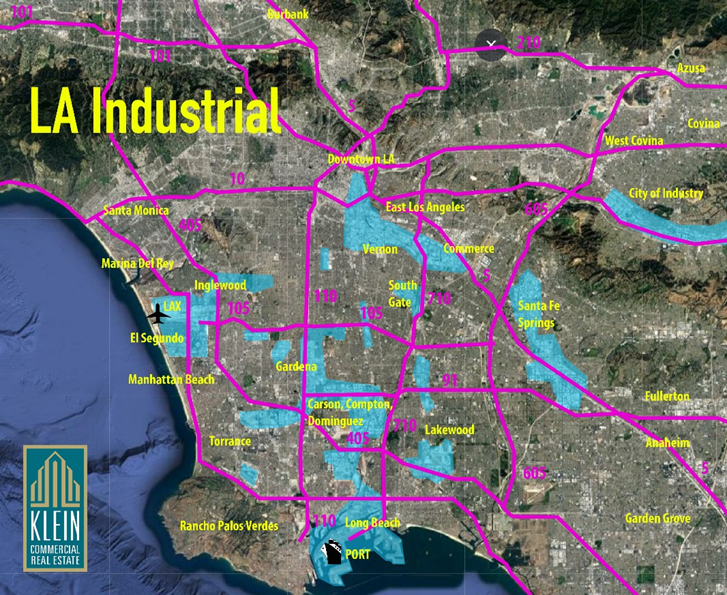

In Los Angeles, industrial real estate has gone from frothy to flat. Rents are in decline, sale prices are down, and to the consternation of many sellers, investors have a “large margin of safety” when they make an offer. There is a wide variety of buildings available, especially for warehouse and distribution. One segment of shortage is modern, free-standing, and secure industrial buildings that can meet government clearance. Power and parking are needed for tech-industrial. Multi-tenant units, too, are in short supply.

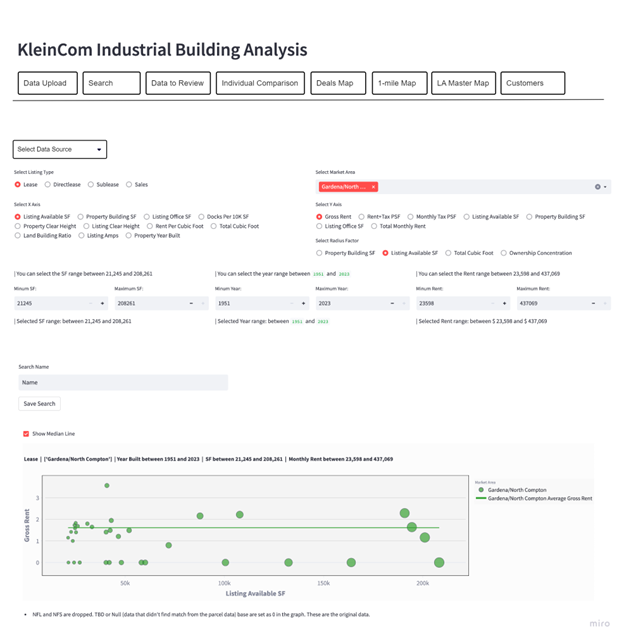

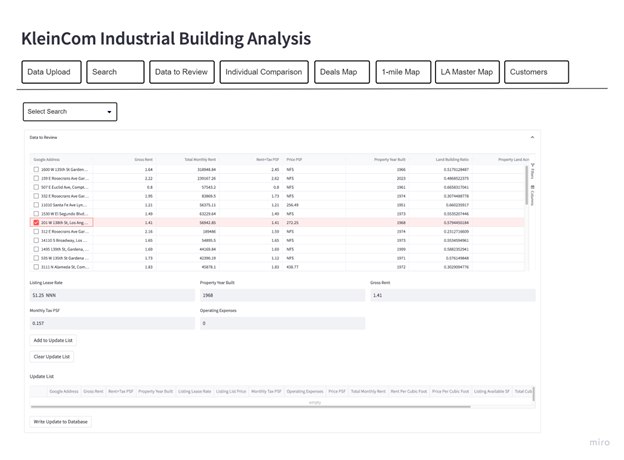

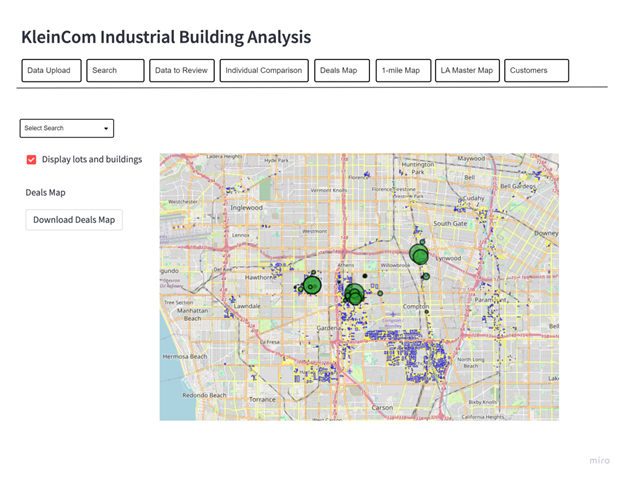

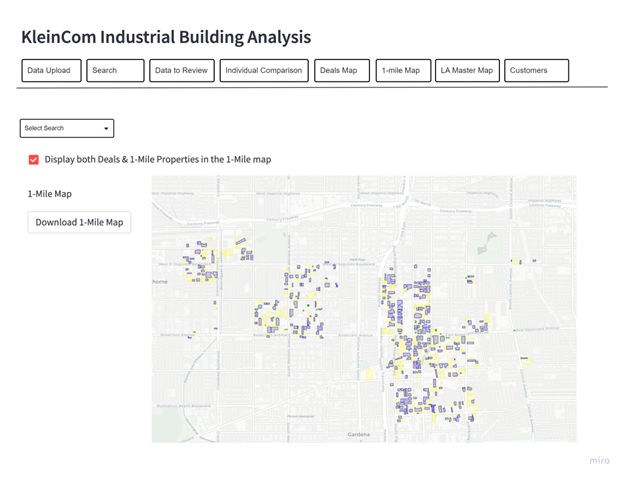

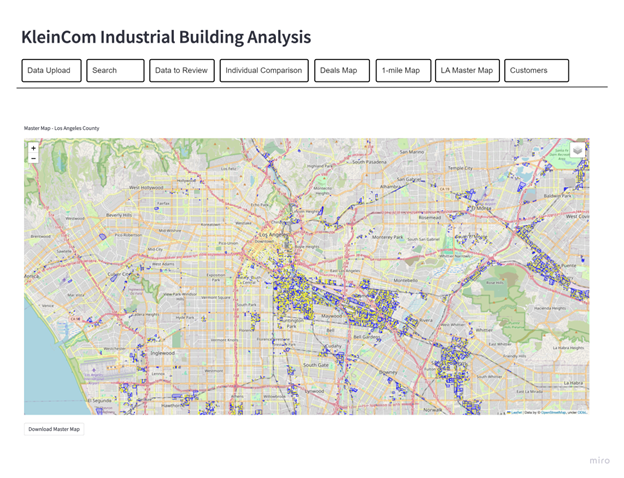

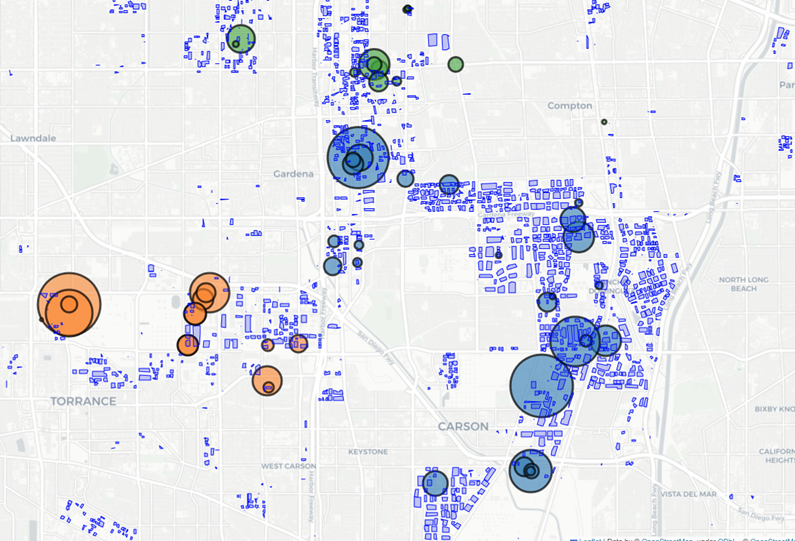

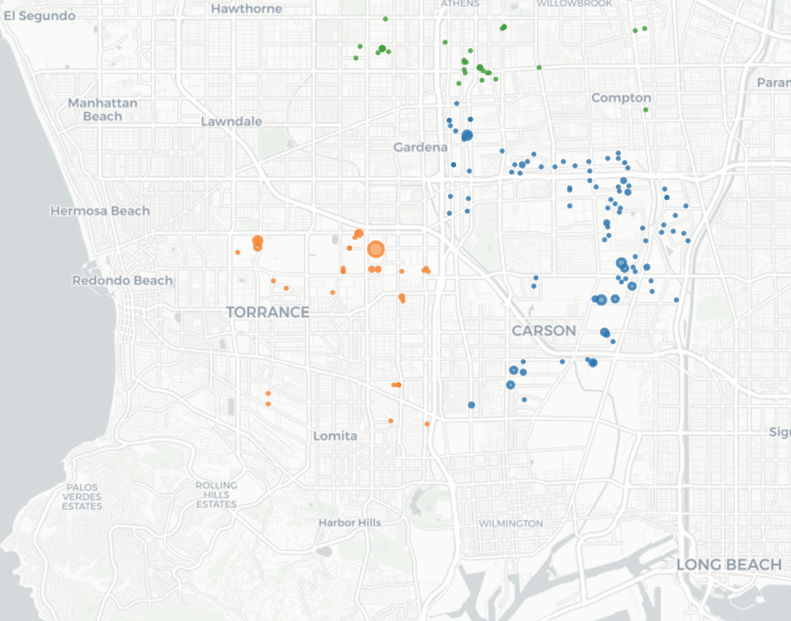

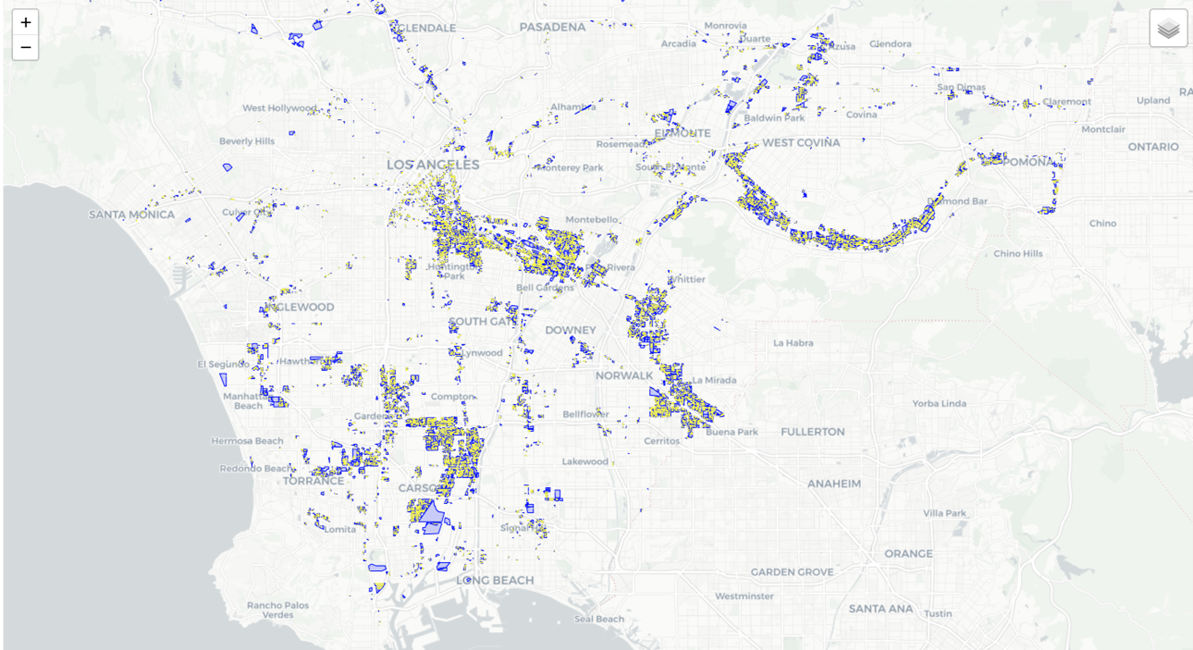

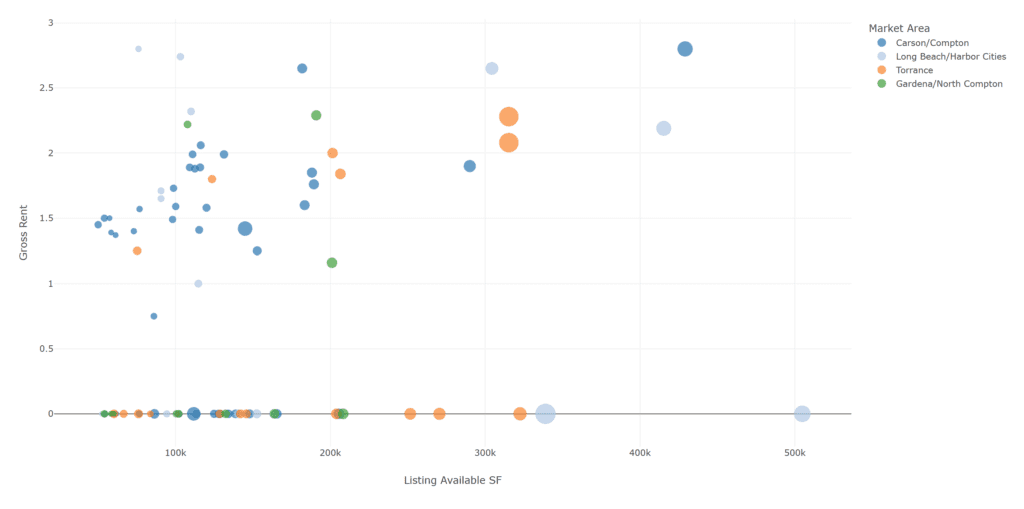

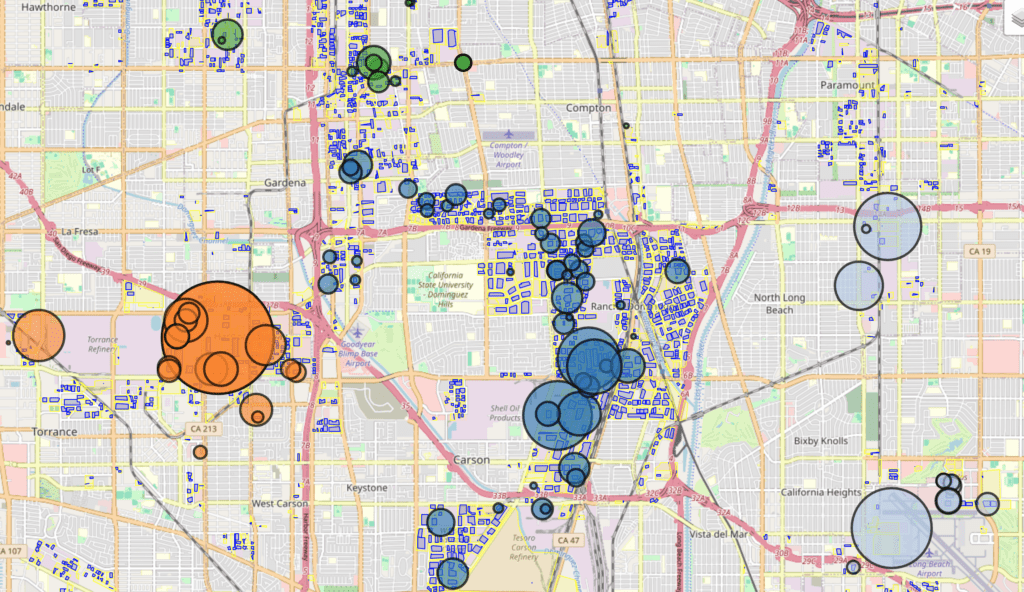

We create analytics and compare buildings based on attributes and location. Clients can understand the real estate markets by scrolling over and seeing the metadata for each property. We create graphs for tenants, owners, and investors. Originally coded for Streamlit, we migrated to a SQL database and then to Postgres so we could capture location data. We’ll be able to solve some nagging problems with this next revision. Organizing market data in this, or other ways, is a necessary step for adopting new standards.

Our staff has grown to eight people split between sales and administration. We have a 45-year history in South Bay industrial real estate and an office in Gardena for most of that time. We live on deals. Please contact us if we can help with your next industrial deal. In Los Angeles, or anywhere in the U.S.