From Vibe Coding to Deal Making

|

|

From Vibe Coding to Deal Intelligence: How One LA Broker is Quietly Building a Tech Edge

The barrier between “having an idea” and “having a working tool” has essentially collapsed. Most commercial real estate brokers haven’t noticed yet. Jim Klein has.

Klein, an industrial real estate specialist in the Los Angeles market and a seasoned SIOR member, has spent the past stretch of time doing something most brokers his caliber rarely do: building his own technology stack. Not by hiring developers. Not by purchasing enterprise PropTech subscriptions. By sitting down with AI tools and describing, in plain English, exactly what he needs and watching functional software materialize in response.

It’s a practice gaining traction in tech circles under the name vibe coding, and it may be one of the most underappreciated skill sets a commercial broker can develop right now.

The Broker-Builder

There’s a new archetype emerging in commercial real estate. Not a technologist. Not a software entrepreneur. Just a seasoned practitioner who got curious, leaned in, and discovered that building useful tools no longer requires knowing how to code.

Vibe coding works exactly the way it sounds. You describe what you want to an AI. The AI writes the code. You refine it through conversation. You deploy it. The “coding language,” as Jim puts it, is basic English and that’s precisely what makes it accessible to anyone willing to try.

He offers one honest caveat worth passing along: having someone with a programming background nearby during those early sessions helps clear the initial hurdles. The fundamentals of how scripts connect to platforms and APIs aren’t always intuitive the first time. But once you’re past that threshold, the playing field levels quickly and the possibilities expand fast.

Two Platforms, Two Distinct Superpowers

What makes Jim’s approach particularly instructive isn’t just that he’s using AI. It’s how deliberately he’s matched the right tool to the right job. He’s built a two-platform intelligence system, each one purpose-designed for a different dimension of his business.

Gemini: The Market Radar

Jim has configured Google’s Gemini as a live intelligence feed for the industrial sector. Every day, it pulls news from sources around the globe, publications and Google Alerts he’s personally curated, and filters everything through a custom keyword ranking system. Words like expansion, growth, layoffs, WARN notice, and default trigger prioritization, automatically surfacing the stories most likely to signal a leasing event, a distress opportunity, or a tenant in motion before the broader market catches on.

What elevates this beyond a standard news aggregator is the Google Maps API integration. Every story arrives with precise location data attached. A logistics company announcing expansion in the Inland Empire isn’t just a headline. It’s a pin on a map, a radius search waiting to happen, a prospecting call that can be made before a competitor has even seen the news.

The infrastructure behind all of this? Google Workspace. Gmail. Sheets. Calendar. Docs. Tools every broker already has open on their desktop every day. What Jim discovered, and what most brokers haven’t yet, is that every one of these tools has script extensions that can be unlocked through AI-generated code. You describe what you want. The AI writes the script. When something breaks, it debugs itself.

The entire workflow is built on tools you already pay for. The only new ingredient is knowing to ask.

Claude: The Market Intelligence Engine

The second platform in Jim’s stack is Anthropic’s Claude, and here the application shifts from market surveillance to deep market knowledge.

Jim has loaded Claude with Los Angeles parcel data and market comparables, effectively transforming it into a conversational database that would have required a dedicated GIS analyst to replicate just a few years ago. From anywhere, including the field, he can ask:

Answers come back in seconds, often with maps generated on the fly. And this is just the beginning. CRM data integration is next on Jim’s roadmap, meaning contact history, deal activity, and relationship context will soon layer directly on top of the parcel and market intelligence already in place.

This is what a true deal intelligence platform looks like when it’s built by someone who actually understands their market, not by a software company making educated guesses about what brokers need.

The Question Every Broker Should Be Asking

Jim frames the real challenge with characteristic directness:

“How are you making more deals with AI?”

Not “Are you using AI?” By now, almost everyone can check that box in some form. The sharper question is whether AI is actually changing your deal count, your deal quality, or your competitive position. That requires a different level of intentionality than having a ChatGPT account you open occasionally.

Jim’s framework offers a useful benchmark. His AI stack is:

That’s not a technology experiment. That’s a competitive infrastructure.

The Window Is Open, But Not Forever

The early adoption advantage in AI-powered brokerage workflows is available right now. But windows like this don’t stay open indefinitely. The brokers who will look back on this moment as a turning point are the ones treating AI not as a novelty, but as infrastructure to build on. Quietly. Deliberately. Deal by deal.

Jim Klein’s example makes one thing clear: you don’t have to wait for a PropTech company to package this into a product. You don’t need to hire a developer. You need curiosity, a willingness to experiment, and maybe one person nearby who’s been around code before.

The rest, it turns out, you can figure out in plain English.

Jim Klein, SIOR, is a commercial real estate broker specializing in the industrial market in Los Angeles. His work in AI-integrated market intelligence reflects a growing movement among top practitioners applying practical technology to generate measurable business results.

In my early days in the industrial real estate business, information was physical. Listings were delivered in three-hole-punched books, an inch thick, and we were “farm brokers” tethered to small, tightly drawn sub-markets in Los Angeles. If you stepped out of your boundary, you had to bring in a partner who worked that different turf. It was an era of high friction, but it birthed the deep local specialization and clients that stayed with me for decades.

Today, we are in a New Alignment. Two massive shifts are happening simultaneously: a geopolitical fracturing where U.S. bloc industries are “friend-shoring” away from traditional offshore centers, and a technological revolution where AI is partnering with humans to lead us to new directions. A major underpinning of the business, the agency relationship, will diminish as a transaction mindset takes hold. We are facing a reconfiguration of the industrial real estate business.

The New Alignment allows us to have a global view that was previously impossible for a local broker. By mapping industrial infrastructure and supply chains within and across borders, we can see the “fracture” in real-time. Through our domestic and international network of SIOR brokers, we aren’t only looking at filling vacancies; we are examining how a specific property fits into a resilient global network. AI allows us to move beyond the “farm” mentality and into a high-level global network.

A side effect of this shift is that global tools and perspectives make us more aware of the local level. Even as we monitor global trade and production, these same techniques provide a sharper, more granular understanding of our home market. At Mr. Warehouse, we update our location mapping and pricing graphs for the Greater Los Angeles area monthly and offer these analytics to our partners in other markets. It’s a vast improvement from the days of weekly listing books.

AI opens new industrial real markets to explore. And by using what we learned locally, we can partner with our global colleagues to achieve what we couldn’t do alone.

In the “farm broker” days, our data was fixed in a physical book. Today, our data lives with tools that capture intelligence. In the New Alignment, we don’t look only for real estate – although through that is the primary means we are compensated; we look for meaning in infrastructure, supply chain, humanity and how that fits into a model of production and distribution. We measure a central principle in the real estate business – location, location, location – and its impact on finance, operations, and the intangible.

Mr. Warehouse adopts three layers of data. These tools allow us to map out the market with precision, helping occupiers and investors find the “nodes” that will thrive in a fractured economy.

We use the Drupal Geofield module as a simple way to store and map industrial infrastructure location data. The map visualizes location and geographical relationships. By feeding high-resolution parcel-level, ownership and location into the map, we create a transaction platform not only around availabilities, but proximities.

Once we create the physical map, we apply a layer of logic using Streamlit, an analysis software that uses a property database to calculate physical and value relationships for the purpose of making transactions. We turn raw data into meaning. For instance, our Los Angeles industrial data will show the closest and most optimum properties to move. For an occupier, this layer shows if a given site will optimize their supply chain or if they need to replicate their business, or a part of it, in a more efficient manner or hub.

The most powerful data structure we have isn’t digital—it’s human. After 45 years in the business, with most of those years as an SIOR and attending over 65 conferences, our network of relationships is a living social map domestically and internationally. We use modern social networks and our Global SIOR partners to enhance our technology. It’s a privilege for me to work with the best in the business. This layer turns “data points” into “handshakes.”

In the industrial real estate business, the fundamentals haven’t changed in nearly half a century. Location is primary. Occupiers will always want to improve their business. Investors want a reasonable financial reward for taking on real estate risk. What is changing is how humans use machines and how artificial intelligence can serve, not as a tool, but a guide.

As we embrace the New Alignment, the nature of the relationship between broker and client is evolving. While State Real Estate Licensing Law emphasizes traditional agency relationships in their education and discipline, the reality for sophisticated corporations and institutional buyers is they want a transactional relationship. Clients want high-level intelligence, execution and data-informed results over traditional handholding. We always operate within agency law and focus on transactional success with the speed and precision.

We are utilizing a sophisticated web-and-data stack to achieve these results:

We use technology to understand location and network relationships under the New Alignment. While global in scope, the local becomes more informed. AI and Fragmentation will lead many of our client to succeed and we want to support them using new technologies and fundamental real estate principles. The New Alignment is a period of opportunity.

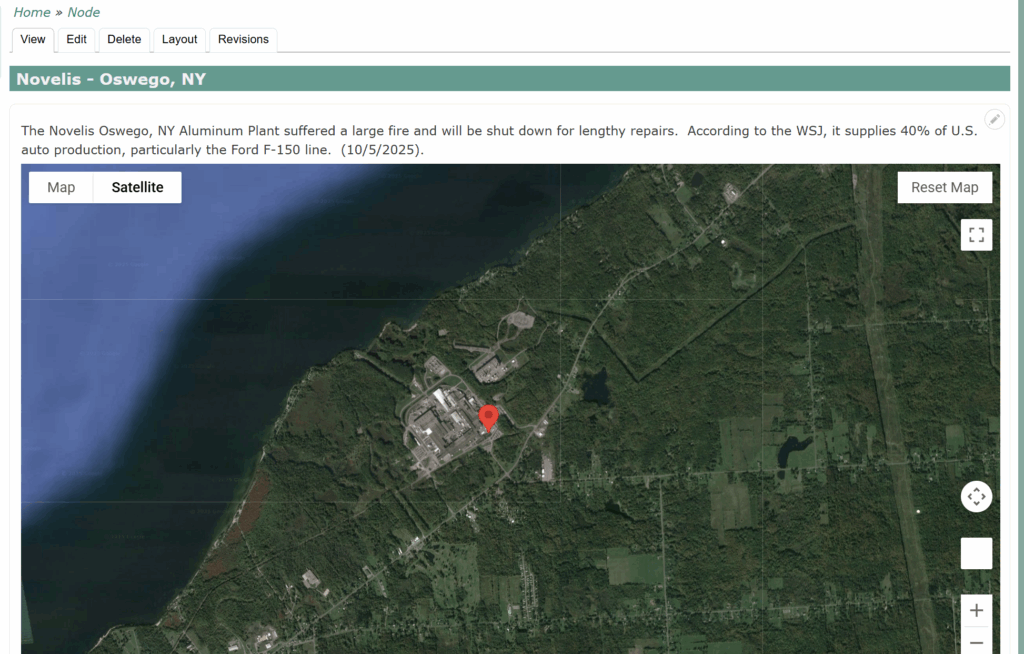

![]()

This plant shutdown caught my attention. The Novelis Plant in Oswego, New York supplies 40% of the aluminum for the U.S. auto industry.

For decades, the U.S. industrial real estate landscape was largely shaped by the flow of consumer goods. e-commerce, brick-and-mortar supply chains, and manufacturer distribution networks. This model is not going away and will be enhanced by more e-commerce. However, a profound shift is now underway. New trade dynamics, tax incentives; and support for AI and Data Centers will re-orient location and capital decisions. There is a new emphasis on factors crucial for enhanced industrial production. This evolution leads to richer set of criteria for assessing location value with an emphasis on network dynamics, supply chain and underlying AI infrastructure.

For companies that are facing real estate decisions, we found the following framework helps you determine the type of move you are most likely to take. The first three type of decisions are accepted as standard procedures in corporate real estate circles. Infrastructure demands, particularly power, connectivity, and location have grown to being singly important.

1. Incremental Growth: Remaining close to core operations and seeking nearby buildings to facilitates organic expansion or infill needs. This strategy prioritizes maintaining local expertise and established networks. Incremental growth is the most common way to expand. Value is based on proximity.

2. Standardization: Particularly relevant for companies taking multiple facilities to support regional markets or industries. This approach emphasizes consistent specifications and operational efficiency across a distributed network.Common examples are consumer products, industrial supply, and data centers.

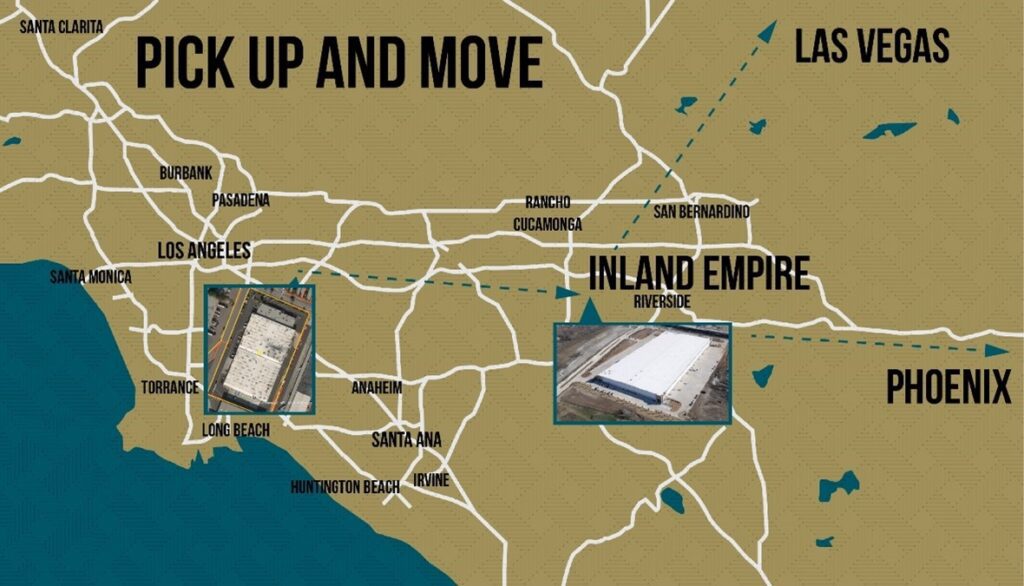

3. Value-Based: Driven by new strategic directions or significant restructuring, this often involves a “Pick Up and Move” to a fundamentally different area, chosen for its long-term alignment with core values and future growth. This frequently occurs when companies leave California for lower costs, fewer regulations or improved synergies with suppliers and customers

4. Infrastructure Dependent: The largest expenditure of industrial development is data centers. Hyperscalers are dependent on huge amounts of power and connectivity on relatively large parcels of heavy industrial land, almost anywhere. Edge data centers are smaller and located in urban centers to serve autonomous vehicles, consumer, shopping, delivery and nearby industrial and commercial facilities.

To support our clients, we developed these strategies over 45 years. We have custom analytics, self-developed maps and personal relationships across North America and Europe. Our diagnostics pinpoint the buildings that are right for you. Please contact us with your questions and comments.

Thank you for Subscribing.

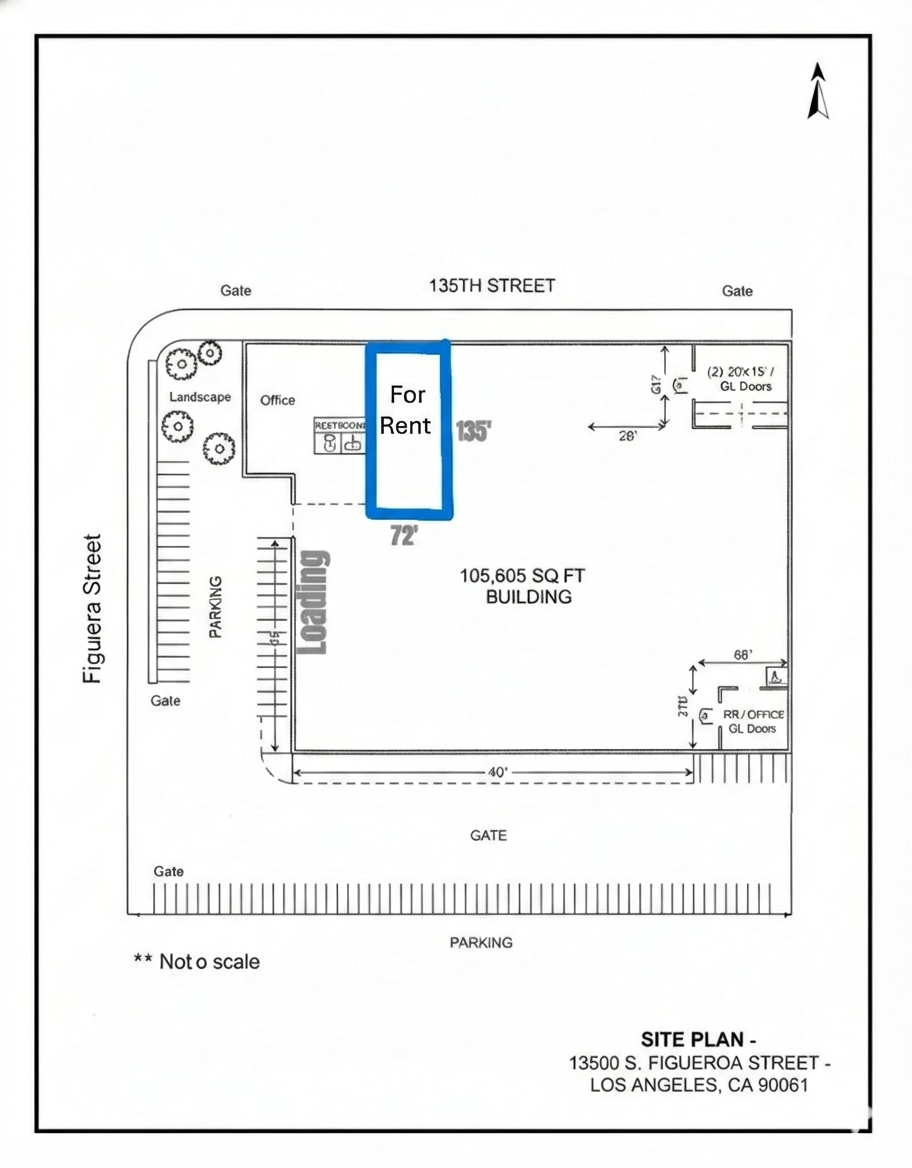

204 W. 131st St, Los Angeles, CA, 90061

Industrial Building for Lease – Now Available

For More Information Please Contact:

Jim Klein, SIOR

(310) 451 – 8121

jimklein@kleincom.com

All information has been obtained from reliable sources, however Property Owner and Broker make no representations as to the information’s accuracy. All tenants and buyers to independently investigate and verify all matters pertaining to the property including but not limited to zoning, physical details, environmental, improvements and any other conditions that affect the Tenant’s or Buyer’s use and occupancy of the property.

Please select a valid form

|

South Bay (L.A.) Industrial Building |

|||

|

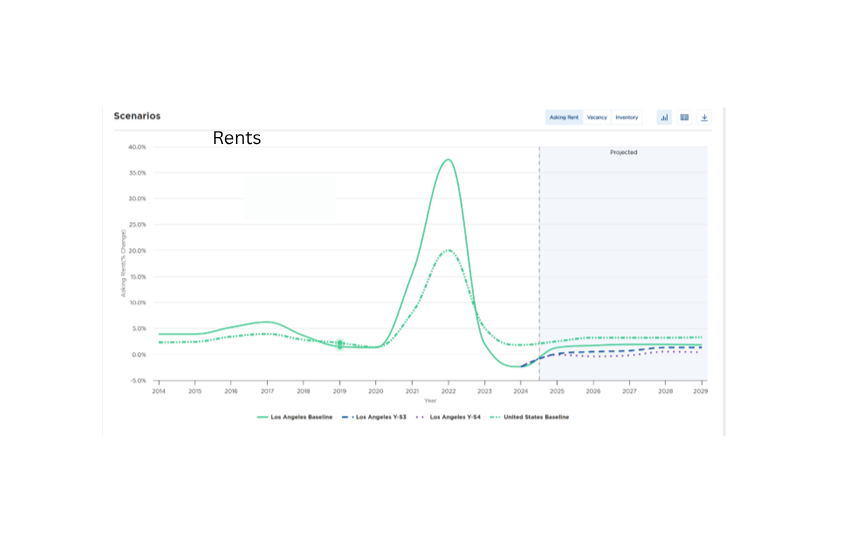

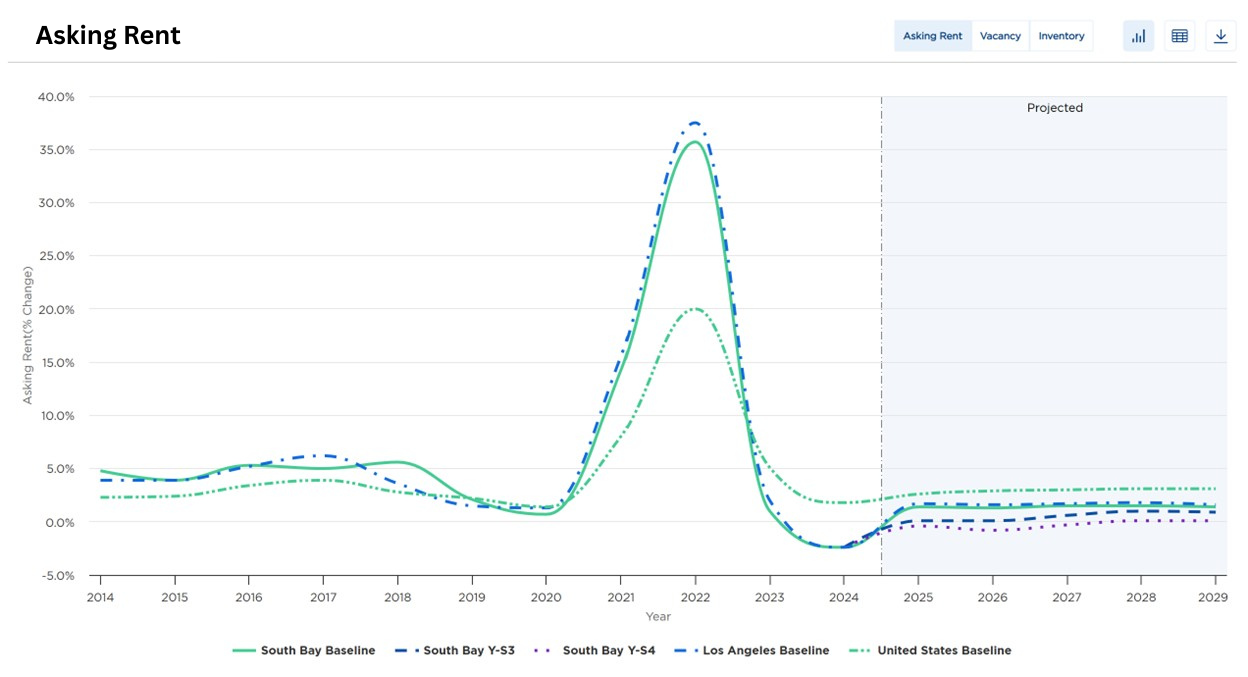

Industrial rents have stayed relatively flat except for a spike during the Covid years. Currently, another adjustment is underway due to a reduction of Chinese goods coming through the L.A./L.B. Ports. The Los Angeles region is a gargantuan warehouse market linked closely and dependent on international trade. |

|

||

|

|

||

|

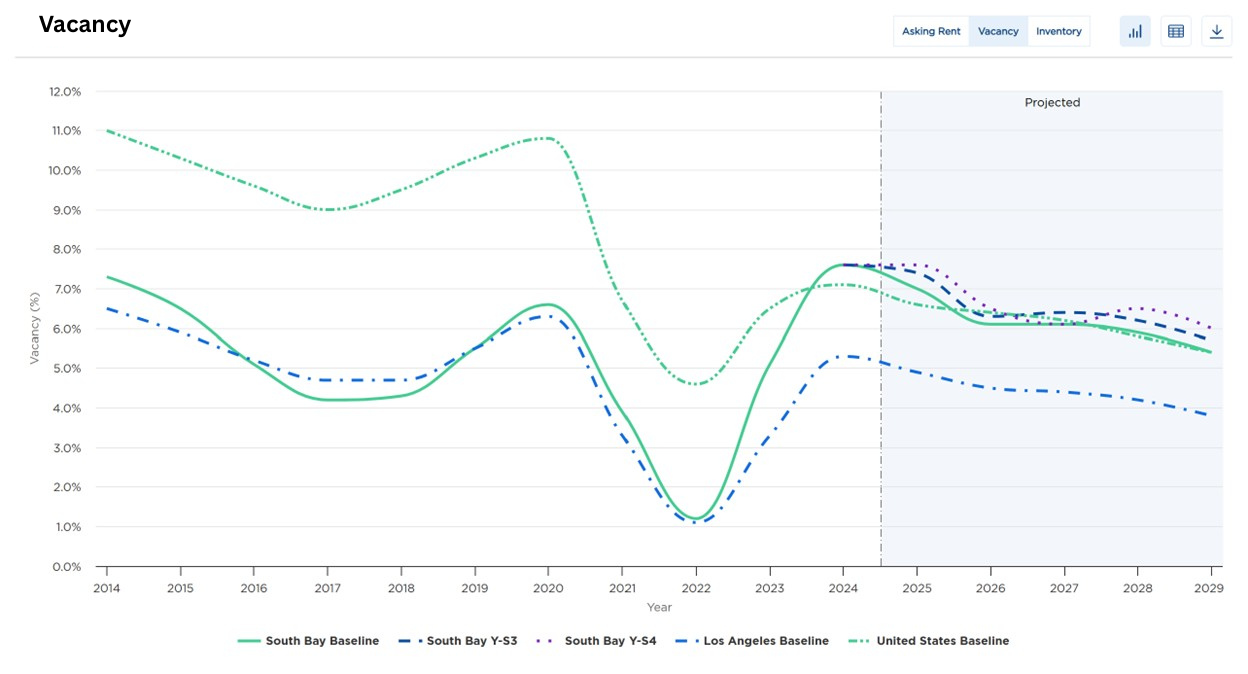

Space availability is increasing because of weak demand. International trade is reduced. One segment that is under-supplied is Hard Tech.Buildings require power, offices, security clearances, parking, cleanliness, and a location along the 405 Corridor. Timing is right to re-position buildings in this corridor. |

|

||

|

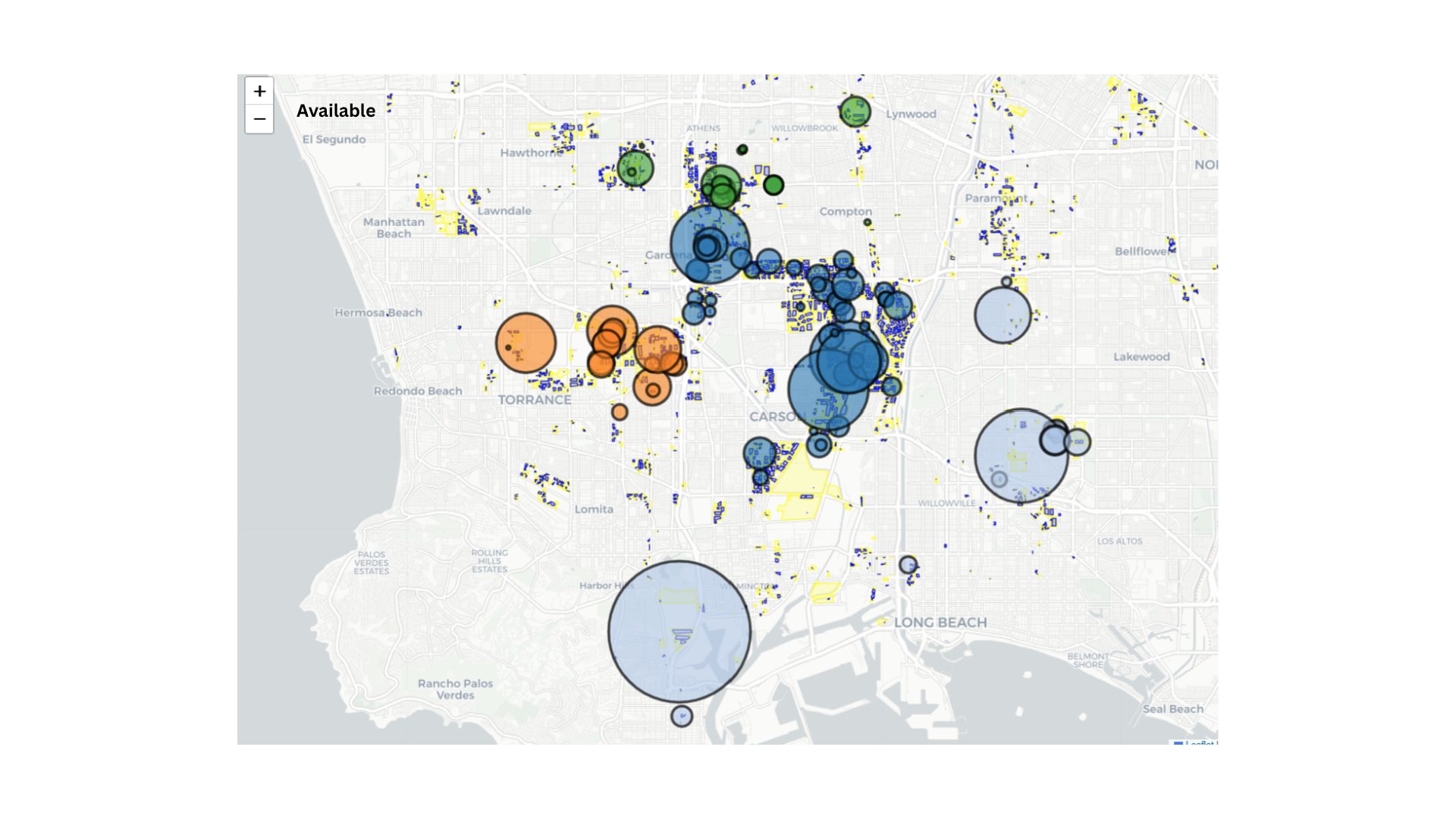

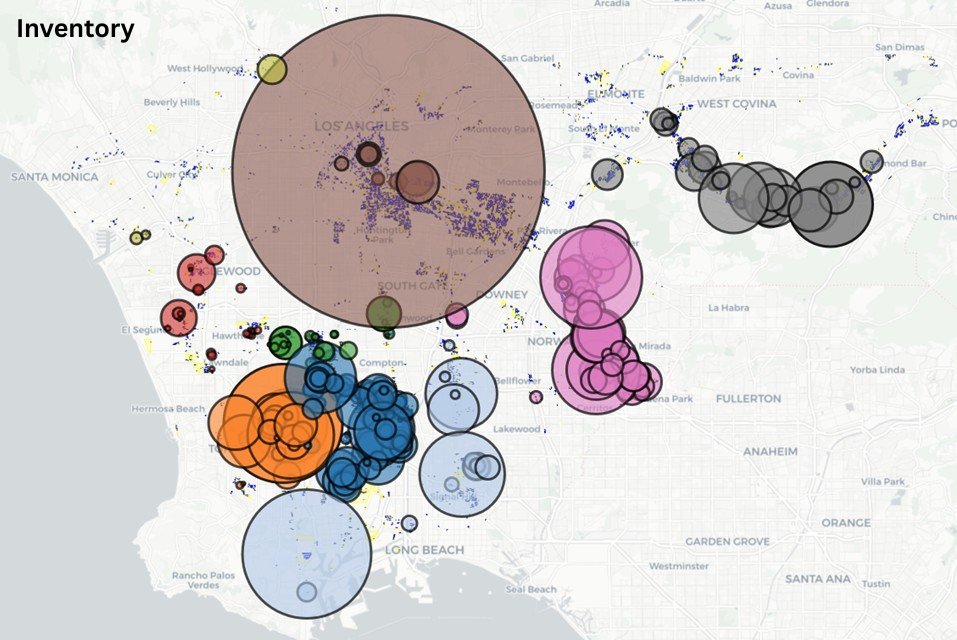

Industrial Clusters |

|||

|

Cluster strategy is used by occupiers to be near skilled employees, vendors, and synergies. El Segundo, the 405 corridor and neighboring cities |

|

||

|

|

||

|

|

More Uncertainty in a Soft Market

As an industrial real estate broker in Los Angeles, we make a living by hustle and personal relationships. Despite our effort, when you step back to analyze, it is the macro influences that are the determinant factors. The Great Financial Crisis drove down interest rates and brought in a wave of institutional investors that purchased almost every available property. These property owners received an additional boost during the Covid period that created a surge of imports and warehouse shortages that increased rents. The economic result was inflation and to combat higher prices, the Fed increased interest rates. This action resulted in reduced investor activity because deals no longer made sense. Now we are facing a Tariff Tantrum that is freezing tenant demand. A few months’ pause in activity wouldn’t be bad except many owners are leveraged and need to service their debt. Each macro event has an unintended consequence on pricing and vacancy.

Los Angeles industrial is particularly dependent on goods coming through San Pedro Bay. During Covid, when there were 100 ships waiting to be unloaded, it created a beneficial rent surge for property owners. Today, with a 70% decrease in port traffic, rents are declining. While obvious in buildings, the clearest example is Industrial Outside Storage (IOS), basically truck yards, which has seen a drop of more than 50%. IOS was the darling of large investors and served as a new property class. However, many of those truck yards remain vacant and were underwritten at much higher rents.

Another source of demand, particularly here in the South Bay, comes from aircraft and defense companies. Its origin in WWII has ebbed and flowed between war and peace. I had one client who made aircraft fasteners and during times of peace, they would store their machinery and lease out the buildings. But during the Korean, Vietnam, and Cold War periods, they would bring out that same machinery and start manufacturing. We are at another similar period with a different breed of defense companies financed by venture capital and not by prime contractors. It’s a growing industry but also hampered by not getting the parts they need from foreign countries. We are also seeing Chinese companies exploring the creation of a manufacturing base in the U.S. with their advanced manufacturing equipment.

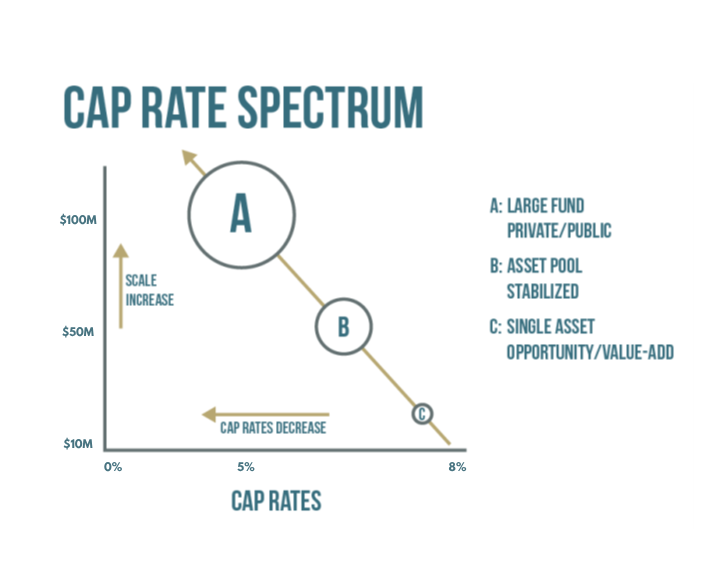

You could say it’s the revenge of the private property owner. During the boom period of low interest rates, competition prevented private owners from affordably purchasing property except through investment vehicles with larger funds. Today, private and long-time owners with a low basis can cut their rents and because of Proposition 13, also have low property taxes. For private owners, they merely need to cover their lifestyle while they wait for better times. Large, newly created funds are faced with valuation cuts that can put them out of business. It’s an unpleasant decision to make, but cutting rents is the way to lease buildings until conditions improve. There are simply too many buildings for lease. Long-time property owners have a clear advantage in today’s market until market conditions change. After all, it’s a cycle.

(The Rent and Vacancy charts are supplied by Moody’s Analytics and are based on their data research and forecast methods. However, they do not account for market sentiment based on current tariff conditions and potential of negotiations. Until trade dynamics become more certain, the current sentiment is unfavorable especially for property owners and tenant’s dependent on import and export activity)