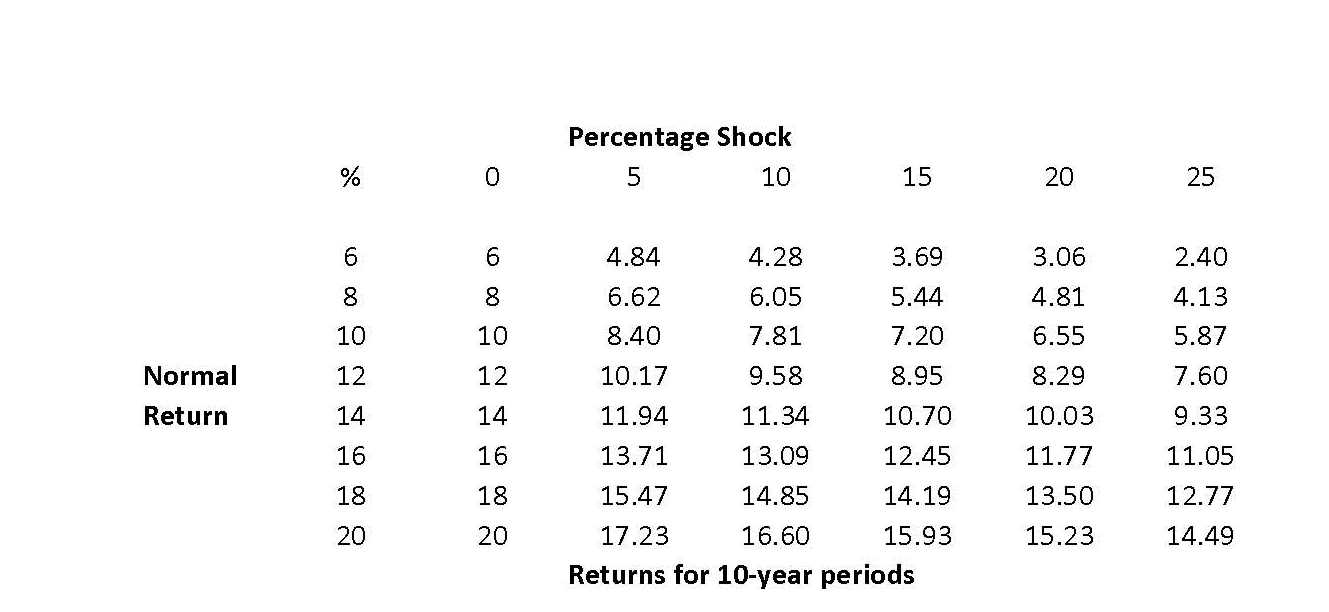

Investment Returns and Systemic Shock

I've reprinted this chart from The Next Convergence by Michael Spence, a Nobel Prize Laureate. While the topic of the book deals mostly with the globalization of economic growth, he spends some time looking at financial shocks and how that partly influences global divergence. One small section of the book looks at periodic systemic risk and how that damages investment returns.

.jpg)

.jpg)