Industrial Building Viewpoint for 2024

There are a lot of industrial buildings available in Los Angeles. It’s a cyclical business and this may be the low point with interest rates projected to decline over 2024. If that’s the case the downturn wasn’t severe. For now, new development will moderate until absorption and lending pick up. Tenants may not see this opportunity for a long time to come. With falling rents, landlords need to close deals fast. If negotiations stall, that tenant will find a cheaper building.

Our analytics show a very healthy supply of buildings between 100,000 square feet and 200,000 square feet. Larger buildings are slightly harder to find because large parcels are rarer in an already developed city. Small spaces are relatively scarce, especially those with power, since there has been very little new construction in that size category for several years. Since rents are greatly influenced by property taxes, we include them when we plot rents. By far the better bargains are with long-term owners, who because of Proposition 13, have significantly lower assessments. Conversely, if you need a new, modern warehouse for high capacity uses, you still need to pay up.

China Gateway

While Los Angeles has a diverse industrial base, much of the development and leasing activity over the past two decades came directly from Chinese goods entering San Pedro Bay. The warehouse business in Southern California and as far away as Central California, Las Vegas and Phoenix have all grown because of Chinese Imports. Declining imports through Los Angeles unquestionably impacts leasing and rental rates.

In only a short period, the growth story of industrial real estate for the past 20 years started when China was admitted to the World Trade Organization. The driving force of industrial real estate was to accommodate Chinese imports with a vast distribution network of North American warehouses and container yards. The ecommerce boom, surging during the Covid period, was another large reason corporates were taking on large chunks of warehouse space. Corporations today are adjusting their needs due to new policies in targeted industries for computer chips, electric vehicles, national defense and import tariffs… And seeking new suppliers away from Chinese chokepoints.

The import amplification during the Covid period caused an outsized snarl in the supply chain. You may recall as many as 105 container ships were waiting along the Sothern California Coast for a berth. The unprecedented backlog is well over and so are the market distortions that came with the import surge. In addition, because of port delays, resiliency, and labor slowdowns, many importers made the permanent decision to shift warehouses away from Southern California to other US ports in the South and East.

Industrial Policy

Outside of Los Angeles and throughout many parts of the U.S., recent tenant demand has been spurred on by a massive, $2.2 Trillion federal industrial policy included in the CHIPS, IRA, Bipartisan Infrastructure Deal and a national defense industrial strategy. This combination of direct grants, subsidies, domestic content rules and friend-shoring has increased industrial building tenancy and development. Unlike organic development that occurred because of open trade, current US industrial policy is heavily supported by political decisions and lobbying. Local leaders take credit for federal subsidies and state incentives that bring employment. There are many published maps that show investment for computer chip plants, EV vehicle production, batteries, defense plants, and other new factories.

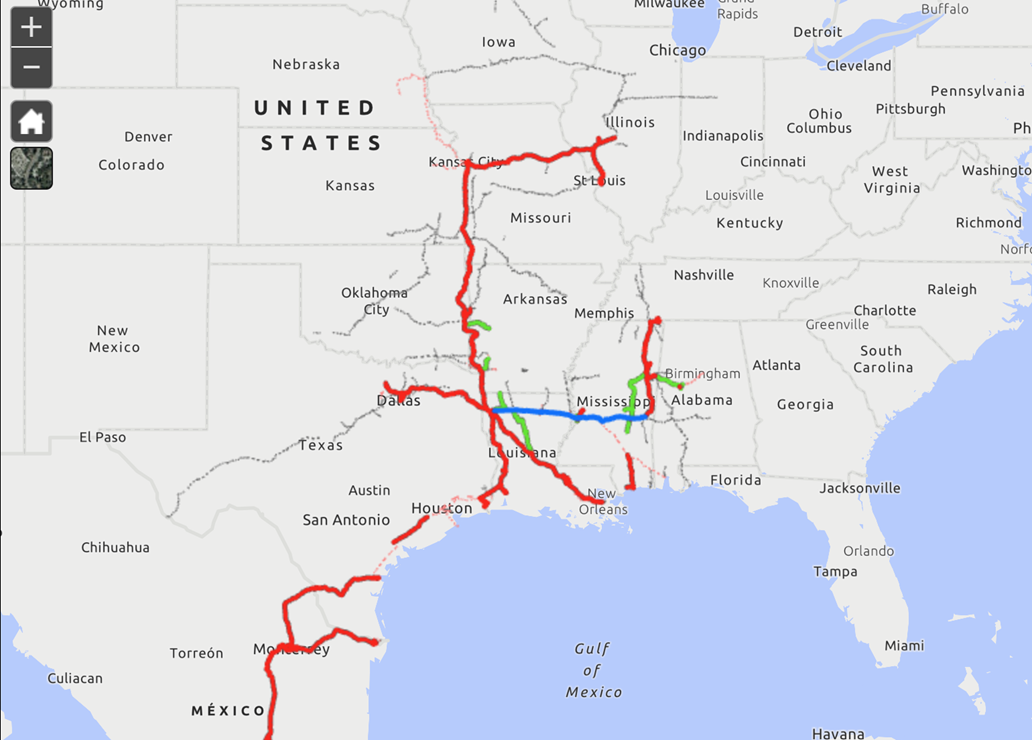

As industrial supply chains adapt, so does the real estate that serves them. Over the past couple of decades, an open market, characterized by Chinese imports, determined the location for industrial building development. This generally meant locations near major container ports received the most interest. In contrast, industrial policy changes trade dynamics by turning to suppliers that will support US national goals. For instance, more manufactured goods are coming through Mexico and creating more traffic for industrial products along the Kansas City Southern Railway (KCS). Monterrey to Houston, Dallas, and Kansas City are new, important links along with many of twin plants across the border towns. Another example is European manufacturers; when they seek to expand in the U.S, Europeans prefer locations in the southeast because of shorter travel times and “right to work” rules.

Interest Rates

For Los Angeles real estate and beyond, the rapid rise of interest rates shook 2023 and put both tenants and the investment/development community in a squeeze. While not historically high, the 250-basis point increase was rapid and caused turbulence for those counting on low rates forever (or at least until they sold their building). Even with a forecast of interest rate reductions in 2024, a higher hurdle rate and an increase in the cost of carrying vacant space will provide more balance between landlord and tenant.

Over the past 15 years, particularly starting in 2008 during the Great Financial Crisis, industrial real estate became financialized as investors searched for advantageous relative returns. It put the traditional owner-user in the position of renting because all the best deals got snapped up by investor/developers. This condition started to moderate in 2023 as normality returned with more opportunities for local business owners to buy their own real estate. Don’t wait too long. There is a new wave of money entering the market. Private wealth managers are seeking alternative investments like industrial real estate. These new buyers will become more apparent as bond yields drop.

Outlook

In our areas of specialty, we see the following:

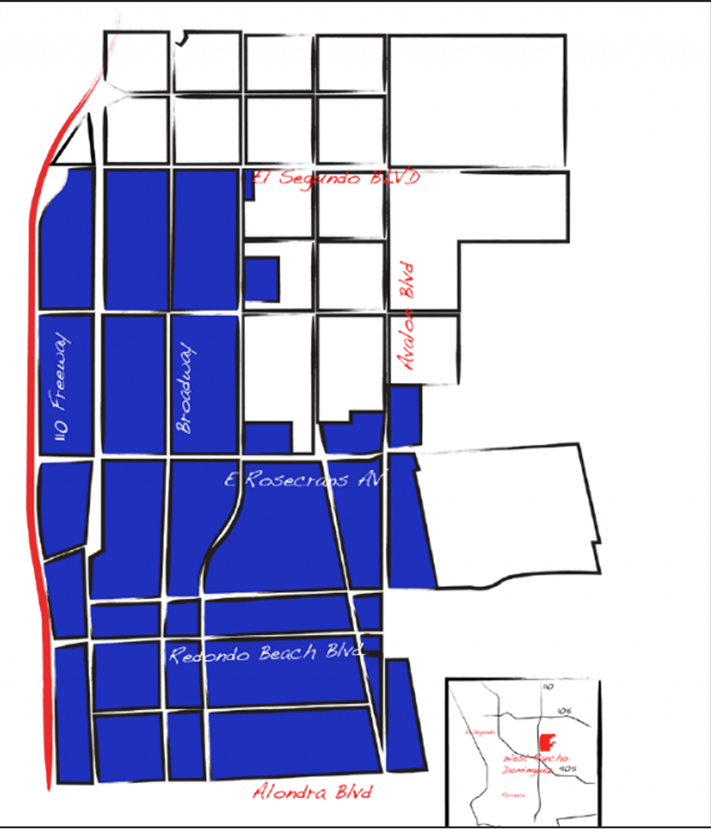

Our traditional “farm area” for over forty years is in the South Bay, particularly Gardena. This also includes Carson, Compton, Torrance, Dominguez and into the Beach Cities and portions of Long Beach. The zip codes 90061 and 90248 are also included and go by several different names, West Rancho Dominguez, East Gardena, Unincorporated County, and my favorite, “The Strip”.

South Bay industrial property is a core holding of every major industrial REIT, Pension Fund and Insurance Company. It’s notable for legendary aviation, electronics, and defense manufacturing companies; vast warehouses serving San Pedro Bay; proximity to L.A.’s transport infrastructure including the twin ports, LAX, Downtown, downtown markets and a dense freeway network. It’s central to labor, executives, and a skilled and educated workforce. The combination of appreciation and rent growth is among the best in the U.S.

One area that deserves special attention is “The Strip”. Over the past few years because of lax policies and enforcement, local Los Angeles government has allowed RV Campers to park on the streets bringing with it crime, squalor, drug dealing, and prostitution. The area smells of human waste and trash. This condition has caused values to plumet and tenants to flee. Finally, at the end of last year, the County started to offer more permanent housing and campers are being removed from several major corridors. While some streets have returned to sanity, if you take a drive on Redondo Beach Boulevard, Avalon Boulevard, 131st Street or Spring Streets, you will see the awful human condition. Local government leaders say they are making progress and in a hopeful start to the New Year, as the RVs are removed, values and tenants will return. Why? Location, of course.

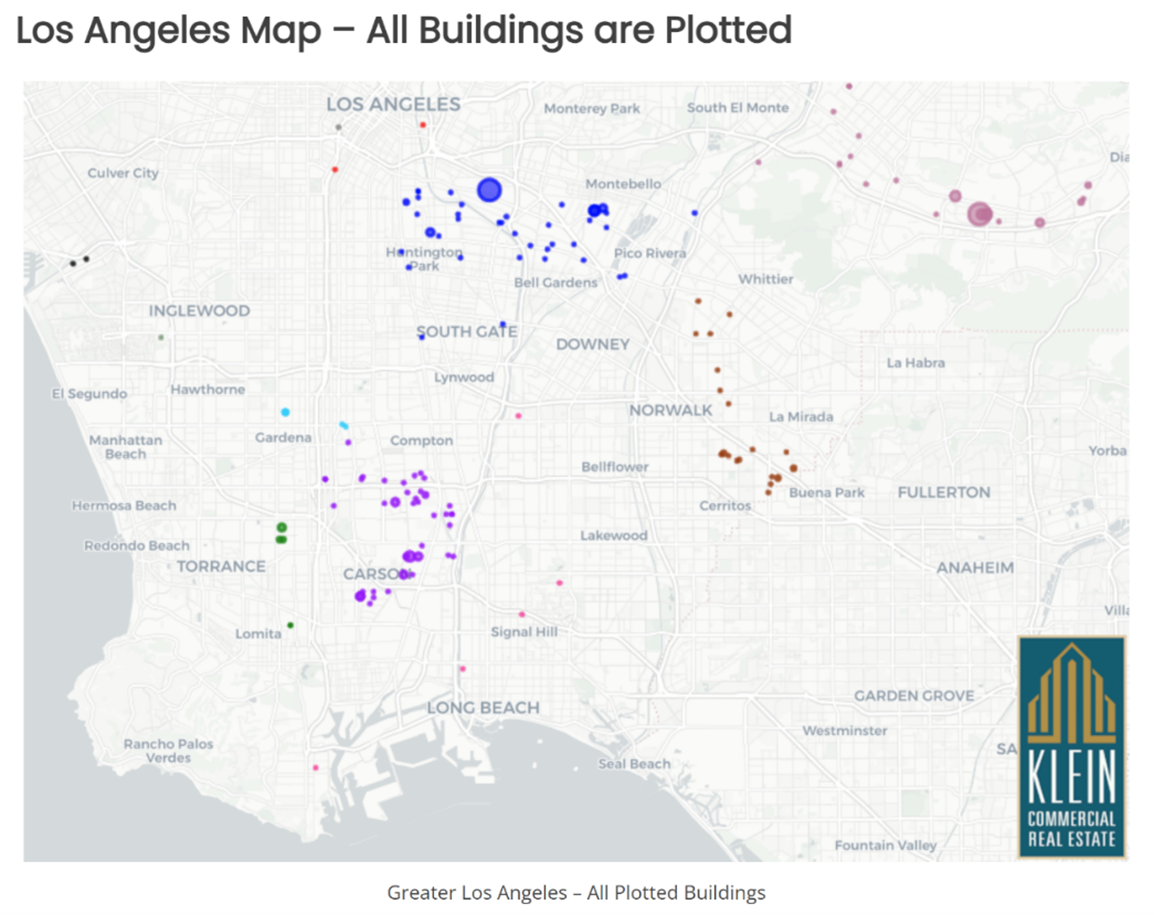

Filling up empty buildings is a goal for 2024. In contrast to recent previous years, vacant industrial building inventory is growing (map above is 50,000 SF and greater). Many new property owners are facing headwinds from the finance markets, and they are motivated to obtain tenants. As prices settle, more tenants will see the opportunity is now! We use experience, analytics, and long-time relationships so clients are assured of the deals they make. As an independent broker, our background in corporate real estate provides a discernable edge in analysis and acumen.

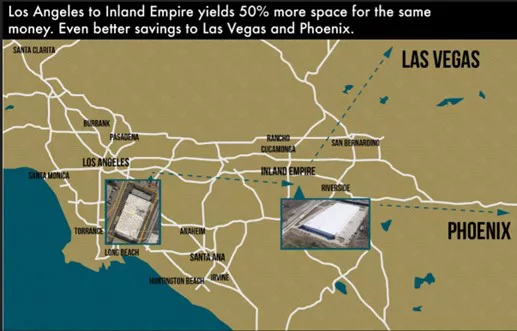

While Los Angeles is the largest industrial building market in the U.S., and when combined with the Inland Empire, Southern California is an industrial behemoth. For many companies, “agglomeration” is the primary reason to be in Greater Los Angeles. However, many businesses continue to seek new horizons to avoid California regulation, politics, and taxation. For those businesses considering leaving California, our SIOR colleagues in the Inland Empire, across the U.S., Canada, Mexico, and Europe have helped many of my customers re-locate and add secondary facilities. In cases when we have the data, we add our analytics and custom program to find “off-market” deals.

One area deserving caution is the newer asset class called Industrial Outside Storage (IOS). It’s been a mainstay of industrial property investment particularly near Gateway markets where imports arrive. Many investors have climbed onboard but the IOS market is heavily dependent on truck/container storage and goods arriving from China. Rents are noticeably declining, and vacancies are growing.