Things Are Changing……

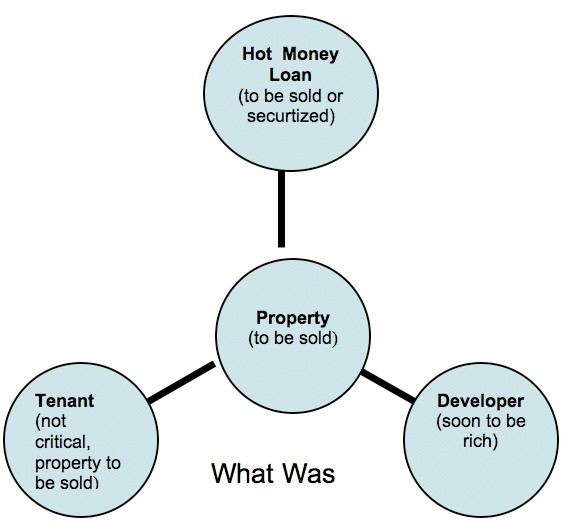

Everyone has an opinion about where we are in the real estate cycle. Home builders and residential lenders see this as a crisis. Commercial brokers nationwide talk about a slow down. Just this month I have seen a lender take over negotiations in a land sale, a substantial money default on a development deal, and a newer investor unable to replace his interest only loan. We are also receiving calls from sellers who passed on our “low” offers earlier in the year and a few landlords are complaining about tenants getting behind in their rent. So far, most of the problems are related to financing and over-optimistic projections. Still, this a lot of personal incidents in a short period.

Continue reading “Things Are Changing……”